The US pet market: an update

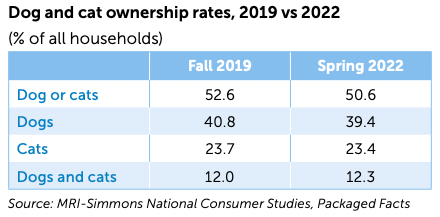

Although the number of US households owning dogs or cats is 2% less than in 2019, the super premium category and increases in e-commerce sales are expected to drive the industry in the near future.

In the wake of COVID-19, a spike in pet ownership among upmarket consumers was offset by declines in pet ownership rates among less prosperous or more budget-conscious households.

Expensive pets

A national gain of 688,000 dog owners with household incomes of $100,000 or more between 2017 and 2019 was followed by a far more dramatic increase of 3.2 million dog owners at this highest income bracket between 2019 and 2021.

This translated to a surge in ownership of the most expensive pets to keep among the most affluent households. In terms of households earning under $30,000, in contrast, a modest national gain of 264,000 pet owners between 2017 and 2019 was followed by a loss of 3.4 million pet owners between 2019 and 2021.

MRI-Simmons data shows the percentage of US households owning dogs or cats in spring 2022 was 50.6%, down from 52.6% in 2019.

Market values up

In keeping with the increase in dog adoption and ownership among upper-income households, pet care spending surged too.

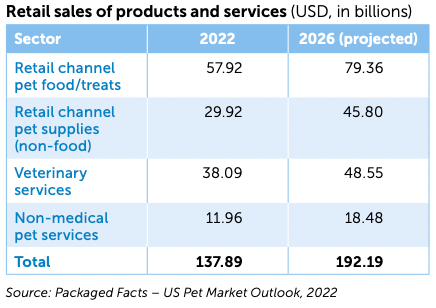

The overall US pet industry, including retail products and pet care services, saw a 14% increase in 2021 – well above the 10% gain of 2020 – with total sales reaching $123.6 billion, according to the American Pet Products Association (APPA).

Looking ahead, the big picture is somewhat tempered for the product and service sectors alike, with Packaged Facts projecting annual percentage gains for the overall market to taper to 8% by 2026.

Inflationary conditions, extended by ongoing supply chain challenges, will continue to compel a portion of less prosperous households to forgo pet ownership or, more commonly, to opt for less expensive pet care options.

With that said, overall US pet market prospects remain robust by any standard, reflecting both the entrenchment of the ‘pets as family’ mindset during this pandemic era and the increasingly affluent skew to pet owner demographics.

Pet market = health and wellness

In tandem with the large role that pets play in our daily lives, a large majority of pet owners are fully aware of the very beneficial impact pets have on their physical and emotional health.

The overall pet market – not just veterinary services – should be considered a health and wellness industry. In this vein, sales of pet food, representing the most important pet health product and two-fifths of the overall pet industry, rose by nearly 16% in 2020 and 15% in 2021.

E-commerce driving sales gains

Packaged Facts projects pet food and treat sales to rise from $58 billion in 2022 to $79 billion by 2026.

Pet food sales gains are being driven only partly by rising food ingredient and distribution costs.

Sharply accelerated by the pandemic, e-commerce has been the medium for pet food market growth, with internet sales of pet products projected to top $38 billion by 2026, more than doubling the 2021 level.

Led by Amazon and Chewy – which account for approximately 46% and 34% of US pet product e-commerce respectively – the internet and its ‘endless shelf’ of product options spurs the ongoing humanization, premiumization and customization of pet food.

Food for older pets

In keeping with an increasing focus on the specific needs of individual pets, only half of pet owners use regular adult pet food formulations.

Packaged Facts’ April 2022 Survey of Pet Owners shows senior/mature as the most popular specialty type of pet food formulation, used by 19% of dog owners and 16% of cat owners.

Weight management formulations, especially associated with older pets, are also an important specialty pet food, given that some 60% of dogs or cats in the US are overweight or obese.

Super premium category diversifying

More specialized pet food types and formulations are driving – and will continue to drive – pet food sales growth. Due to the looseness of the term ‘natural’, and the ubiquity of pet foods positioned in this way, ‘natural’ as a stand-alone benefit peaked several years ago, obliging marketers to segment pet foods into more differentiated types.

Super premium pet food is increasingly mainstream, mimicking human food trends ever more closely. So it has long been clear that the pet food industry would have to premiumize pet food beyond the traditional kibble and wet forms. Freshpet, internet-based DTC start-ups selling fresh pet food (frozen or refrigerated) and ‘human-grade’ marketers are leading the charge.

In addition, as pet food manufacturers ride the humanization/premiumization wave, they are turning their attention more and more to alternative proteins, recognizing that livestock farming is a major contributor to greenhouse gases.

Product packaging is also an increasingly top-of-mind sustainability concern, with recyclable or compostable dry pet food bags emerging in the market. Sustainable packaging for pet food is no longer simply a feel-good or long-term goal, given growing consumer awareness as well as government regulation.

Share this story: