What data tells us about the trajectory of pet food launches

Recent analysis of global and regional trends provides valuable insight into manufacturer activity before, during and since the pandemic.

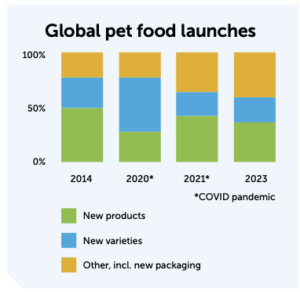

Over the past decade, global pet food launches marked as ‘new’ have steadily declined, data sourced from Mintel GNPD (Global New Products Database) and Mintel Leap, Mintel’s generative AI tool highlights.

Range extensions and packaging

The definition of a new launch is an entirely novel product as opposed to a new flavor, new packaging and so on. These accounted for more than half of all pet food launches in 2014, but dropped to around a third of the launches in 2023.

Shoppers are now being offered a greater array of new varieties, with those increasing from a quarter of total global launches in 2014 to some 40% of launches in 2023. Launches with redesigned packaging have seen a slight increase over the past few years, from 13% of the pet food launches globally in 2014 to 18% in 2023. In Europe, the increase was more considerable – from 9% to 20% in the same period.

General category trends

There is very little difference between cat and dog product launches in terms of the type of launch. And the general trends are seen across the whole pet food category – wet food, dry food and treats.

Pandemic-related drop-offs

New product launches were already declining before the pandemic, but Mintel has identified a sharp drop-off of pure innovation between 2020 and 2021. This was particularly evident in Europe with a sudden decrease in that period from 41% to 34%.

Innovation across APAC

While the global pet market has witnessed a slump in entirely new innovation, things are looking a lot more exciting for pets in the Asia-Pacific (APAC) region, where there’s been a surge of new product development in recent years, including during the pandemic. According to Mintel’s research, about half of launches during 2020-2021 were of completely new products.

Gut health, in particular, has been put in the spotlight, as prebiotic and probiotic claims are seen more in the APAC region. There is also a focus on the composition of pet products, as consumers look for cleaner formulations. This has sparked a growth in ‘no additives or preservatives’ claims.

South Korea is proving to be the star innovator, accounting for 1 in 5 (17%) new products launched in the region over the past 5 years. Alternative proteins feature in some of the more interesting recent product launches, such as brands that contain soldier fly, for example, which is high in protein, minerals, vitamins, essential amino acids and fiber.

China and Japan were similarly active in new product launches, with 14% and 12% respectively.

Cost-of-living crisis impacts Europe

Pet food shoppers in Europe have witnessed the biggest slump in true innovation. Launches marked as new products have dramatically declined, from K two-thirds (66%) of launches in 2014 to just a third (32%) of launches in 2023.

The greatest amount of new product activity was in the UK, which accounts for 1 in 10 European launches over the past 5 years. Here, the cost-of- living crisis has impacted consumer budgets, leading to a definite increase in trading down. Across Europe, many consumers – in attempts to save money – have switched to own-label pet food, cheaper brands of pet food or a cheaper retailer.

Other countries leading in new European product launches are Germany (9.5%) and France (7%). Much of the innovation in Europe features ‘no added sugar’ claims, and this vastly outweighs that of other regions. Some brands are also highlighting the role of veterinarians in the manufacturing stage to reassure pet owners.

Convenient packaging in the Americas

The Americas have seen a substantial increase in new packaging launches over the past decade, from 14% of all new product launches in 2014 to 26% in 2023. Some of this is to offer more convenience – for example the emergence of flexible stand-up pouches.

In North America and Latin America, wellness is taking center stage. Mintel consumer research has found that a significant 61% of US pet owners say that their pet’s happiness and well-being is more important than their own. And 72% of US pet treat purchasers say they like to give their pets different kinds of treat products.

Despite signs of more pet allergies in the region, claims of low, no or reduced allergens have been seen less in the past year. But there are brands that recognize the importance of allergies claiming they can support immunity and the digestive function, as well as providing food and seasonal allergies relief.

Product development outside the box

While innovation has taken a backseat in recent years, there are 3 areas of opportunity for the pet food category.

Inspiration from baby food

Brands designing products for puppies and kittens should take inspiration from the baby food category. This could involve aspects of packaging design, format and materials, or creating food bonding moments.

Justifying sustainable options

Younger pet owners are deprioritizing sustainable pet food due to money concerns. Private labels should venture further into insect-based and plant-based options, while brands can hit the taste and health mark through blends.

The next step in digestive health

Pet owners continue to prioritize gut health when evaluating pet food features. Consumers link the gut with many different strands of health, and pet food brands will similarly make associations between postbiotics and health benefits.

Share this story: