Bright future predicted for private labels

The in-house brand pet food sector is flourishing – particularly in Europe where it often registers higher shares of the market compared to other product categories.

With rising numbers of pet households across the world, and consumers looking for affordable options to feed their pets, retailers have good reason to expand their lines. The latest data provides evidence of how things are developing in this segment.

Global expansion fuels growth

Pet ownership has grown globally, especially since the COVID pandemic. In the US, 51% of households own a dog, while 37% have at least 1 cat. Some 94 million households now have a pet, an increase of 12 million since 2023, according to the American Pet Products Association (APPA).

A total of 340 million households in Europe are pet owners, with 105 million cats and 91 million dogs in European homes. With the growth in household pets, store brands have reaped the benefits. In the US, pet care private label sales reached $5.5 billion (€4.7B) in the 52 weeks to 13 July 2025. This is an increase of 2.4% against the same period of 2023-2024.

US and European numbers

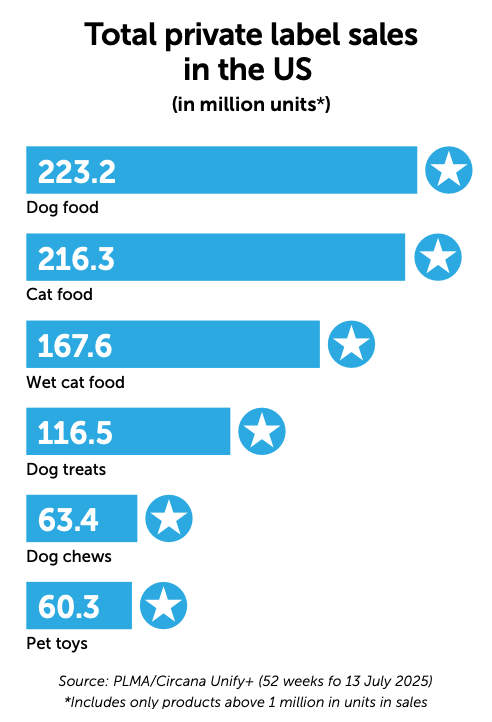

Some of the largest private label categories in the US include dog food ($1.3 billion/€1.1B – 12.6% share), dog treats ($1.1 billion/€0.9B – 22.2% share) and pet toys ($262.7 million/€224.9M – 37.5% share). In unit sales, dog food (223 million – 18.3% share), cat food (216 million – 10% share) and dog treats and chews (180 million – 24.7% share) also reflect the popularity of pet products among US consumers.

This pales in comparison to Europe, however, where private label pet food sales now have some of the highest penetrations among the sales tracked by the Private Label Manufacturers Association (PLMA) and NielsenIQ in 17 countries.

Comparison with branded products

In private label overall volume and value share, pet food is strong when it comes to category sales volume. For the 3 months to 26 May 2025, 13 of the countries tracked by PLMA and NielsenIQ had a volume share of 40% or more.

Portugal (71.5%), Hungary (69.7%) and Greece (66.3%) lead the way in share of unit sales. In value, 7 of the 17 countries have a private label share of over 40%, with 3 of them above 50% – Portugal (53.2%), Greece (50.5%) and Spain (50.3%).

Share vs other categories

The PLMA Sales Dashboard tracks 11 categories, including alcoholic beverages, confectionary and snacks, ambient food, frozen food, health and beauty, healthcare, homecare, nonalcoholic beverages, paper products and pet food. The private label share in the pet food category is often among a country’s top-ranking ones.

Own label pet food products have the top share of all categories in private label sales volume in 4 countries: Hungary (69.7%), Greece (66.3%), Denmark (63.5%) and the Czech Republic (59.1%). In Austria (61.8%) and Poland (52.3%), pet food ranks second behind paper products. Overall, private label pet food sales are in the top 5 private label sales volumes in 13 of the 17 countries tracked by PLMA.

A similar picture can be seen in sales value. In Greece, own label pet food sales rank first in the 11 categories, with a 50.5% share. Hungary and the Czech Republic come second, with 45.6% and 37.6% respectively. Strong sales are also seen in Denmark (47.4%) and Poland (43.1%), where pet food is in third place. Overall, private label pet food ranks in the top 5 in sales value in 11 of the 17 countries.

Further opportunity for advances

Although all this might seem to indicate that growth in private label has reached a peak, which might suggest a lack of opportunity for future growth, the most recent numbers tell a different story. Since 2023, pet food sales for store brands have experienced growth in 10 of the 17 countries in volume share and in 6 of the 17 countries in value share.

The Czech Republic has grown the most, with a 4.1% increase in volume during this period, followed by Switzerland (+2.7%), Greece (+2.4%) and Sweden (+2.1%). This is especially interesting given that Sweden (11.4%) and Switzerland (40.3%) have the lowest private label volume share of pet food, but the numbers demonstrate its promise as a growing category.

In value, there is a similar picture. Denmark has seen an increase of 4.2% since 2023 in pet food sales, while France (+1.5%), the Czech Republic (+1.3%) and Sweden (+1.1%) have also shown steady growth. Once again, France – with 24% – and Sweden – with 6.9% – have 2 of the lowest penetration rates for private label sales value, but growth reflects the potential for store brand products to win over consumers.

US expansions and launches

Perhaps the best indicator of private label growth for pet products comes from retailers on both sides of the Atlantic. In the US in the past 6 months both Target and Associated Wholesale Grocers (AWG), which operates over 3,400 independent stores, have made major announcements.

Retail giant Target has announced it is redesigning its Boots & Barkley pet line and is also adding 150 new products to the line, which was launched in 2011.

In a press release, Amanda Nusz, Target’s Senior Vice President of Merchandising, Essentials and Beauty, said that 70% of Target customers own pets and 30% of shoppers purchase pet products from them: “The new Boots & Barkley reflects our focus on high-quality, stylish and affordable pet accessories that help our guests treat, celebrate and connect with their furry family members.”

AWG, meanwhile, is just entering the private label pet product market with the launch of Pure Wonder by Best Choice. It has debuted with 80 products. The company promises the products will be high quality but also provide value for consumers.

European brands join the club

In Europe, the retail sector is also focusing its efforts on the pet market. Recently, German retailer Kaufland launched its first private label premium pet food brand in its stores under its K-Carinura line, which now offers over 85 high-quality products.

This has been so successful that Kaufland is now expanding, with the K-Carinura Naturals product line promising no preservatives, grains, sugar or colorings. Currently, this new line includes over 30 products, but the company plans to expand to over 60 items.

Other companies are extending their pet product offerings with new stores and dedicated programs. The REWE Group in Germany has announced that its ZooRoyal pet store company is expanding nationwide in 2026. While no exact number has been released, the rollout is expected to be in double digits.

In Spain, Carrefour has launched the Pet Club, which Carrefour Club members can access through an app. Benefits include up to 5% savings on pet food purchases, free access to digital passport services and a veterinary chat with Petpass, funded by Carrefour Club.

Another Spanish retailer, DIA, has added almost 60 products to its Deligato and Deliperro private label pet lines – dry and wet pet food endorsed by veterinarians.

Pets and their humans

Some major pet retailers in the US have also recently announced the addition of private label pet products and, in a twist, products for their owners. Pet superstore chain PetSmart, for example, has introduced the Thrills & Chills collection, which features a variety of Halloween items for pets and includes an assortment of costumes, apparel, accessories, toys and treats.

Meanwhile, Petco is also expanding its product range in a new direction, with the launch of a collection designed for use by pet parents. The My Human line is a selection of pet-themed products, including apparel, decor for the home and workplace, games, toys, accessories and seasonal items.

The pet world according to the experts

The future for pet sector sales overall looks promising. According to the European pet food industry body FEDIAF, sales of pet products are projected to grow by 4.1% in Europe by the year 2026. This growth could come from the increasing demand for organic and free-from pet food, as more owners seem to want to ensure the health of their pets and reduce the number of processed foods in their pet’s diet.

According to Euromonitor, the Asia-Pacific pet care market reached $29 billion (€24.8B) in 2024, making it the third-largest pet market in the world. Euromonitor expects sales growth there to be around 4% in the next 5 years, keeping pace with growth in the US and Europe. This is not surprising, as pet adoption has skyrocketed in Asia during the past decade.

According to a report by Allianz Global Investors, 60% of the population in the Asia-Pacific region now has a pet at home. Investment bank Goldman Sachs projects this to be especially true for China, expecting 8% pet food growth in China over the next 5 years. There is good reason to see why this might be possible. In China, dog and cat ownership is now at 22% of households, or a total of 120 million according to iMedia Research. In addition, 60% of Gen Z are expected to adopt pets in the future.

The rise of Gen Z pet ownership is not limited to China. According to APPA, the fastest growing generation of pet owners in the US is Gen Z. Over 18 million Gen Z households now own a pet, with 70% of households reporting more than 1 pet, making it the largest multi-pet-owning demographic.

Share this story: