COVID-19 and developments in the US pet market

2020 was a unique year for the US pet care industry. Despite the challenges presented by COVID-19, it performed quite well.

Sales growth

Retail volume sales for dog and cat food increased by 4.5%, compared to 2% growth in 2019. Value sales growth was 5.7% in 2020, down only slightly compared to 2019 growth. The impact of COVID-19 on the US pet care industry can be seen in three main areas – reflecting both the time and money pet owners have available as well as the pandemic’s effect on their shopping behaviour.

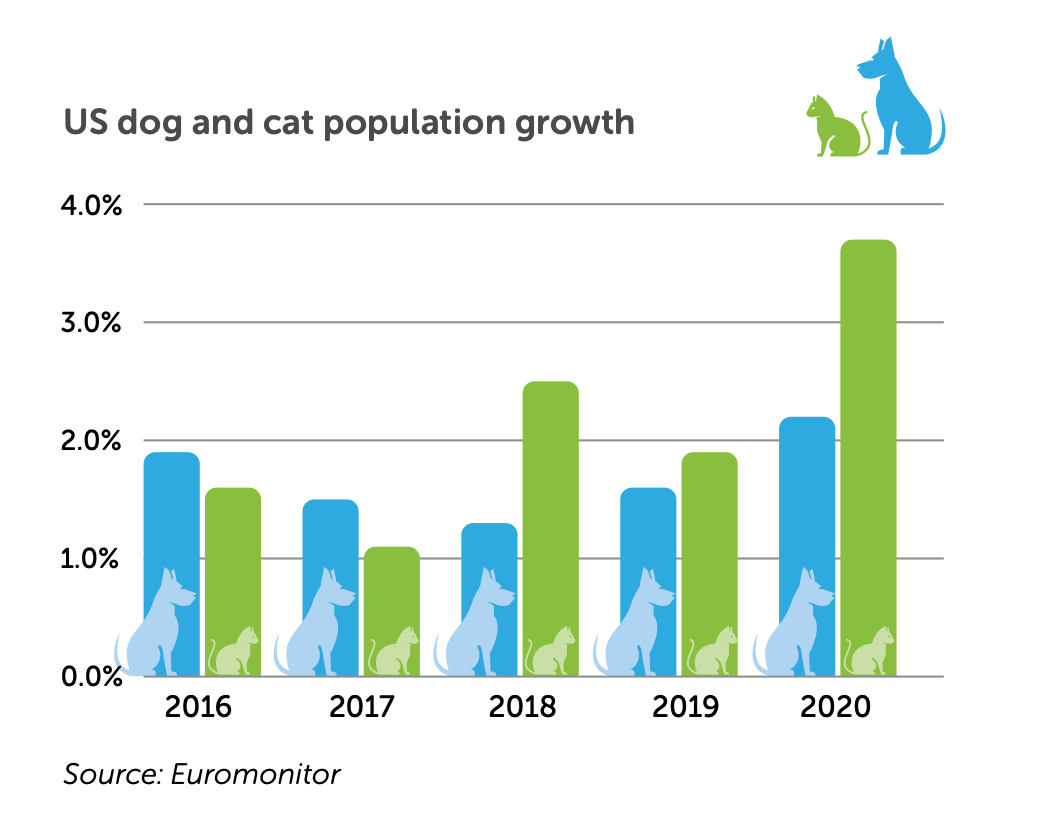

Pet population

One of the most important drivers behind the increased pet food volume last year was growth in the US pet population. With many companies switching to remote work, quarantine restrictions in different parts of the country and a general fear of virus exposure, Americans spent a huge amount of time at home in 2020.

For many, this has been a stressful and lonely time, so consumers have decided to adopt pets in search of companionship. The extra time at home has also been viewed by aspiring pet owners as an opportunity – while pet ownership may have seemed daunting in the past, they now have more time than ever before to train and care for their new pets.

Humanisation and premiumisation

For years, US consumers have shown an increasing willingness to spend more money on their pets. The key shift here is a change in pet owners’ attitudes – pets are increasingly viewed as valued members of the family. This can be seen clearly in the types of pet food and products that have become ubiquitous in the industry: refrigerated fresh food, CBD treats, and weighted blankets are all commonplace in an industry that has been impacted heavily by humanisation trends.

COVID-19 has led to economic hardship for many Americans. Despite this, pet food remains pretty resilient in the face of an economic recession. Premium brands continue to outperform mid-tier and economy brands. Generally, consumers do not want to trade down to lower quality food, even if it saves money. They might even be willing to sacrifice the quality of their own food before they make a change to their pet’s diet. So, while some pet owners needed to seek out cheaper food options, many remained loyal to their same trusted brands in 2020, although a significant portion of consumers turned to mid-tier and private label brands in search of better value for money.

Retail channel shifts

In addition to changing the types of pet products purchased in 2020, COVID-19 changed where consumers bought them. Fearing exposure to the virus, many US consumers turned to e-commerce for everyday purchases. With fast shipping and frequent discounts to be found online, a lot of pet owners opted to buy pet food and pet products from internet retailers like Amazon and Chewy. Auto-ship and subscription programmes increased in popularity, as did click-and-collect programmes that allow consumers to purchase online and pick up orders at a store without leaving their cars.

E-commerce is not the only channel to experience the effect of COVID-19. Pet specialty stores and vet clinics struggled, while larger mass retailers gained share in 2020. For those consumers who are comfortable entering stores to do their shopping, many prefer to at least limit the number of stores they go to. Rather than making a separate trip to a pet shop, consumers are choosing to buy pet food at mass retailers where they can buy groceries and other products at the same time. Since many premium brands have launched in the mass channel over the last few years, consumers do not feel limited by shopping for pet food outside the pet specialty channel.