How is the US pet accessories market performing?

The pet owner’s wallet faces continued pressure – something that is particularly noticeable in non-essential categories such as hard goods. Meanwhile, direct-to-consumer (DTC) brands are challenging traditional retail.

Based on its studies in the US pet category, Cleveland Research Company (CRC) currently anticipates that underlying market trends such as benign inflation, non-essential spending pressures and a slowdown in pet household formation are likely to persist through the first half of next year.

Hard goods having a tough time

One of the largest categories within pet retail – hard goods – is a key topic within research conducted by CRC.

Results show that demand for hard goods and accessories has remained largely muted throughout the year. Category growth for 2024 is expected to be 0-1%, with a similar trajectory forecast for 2025.

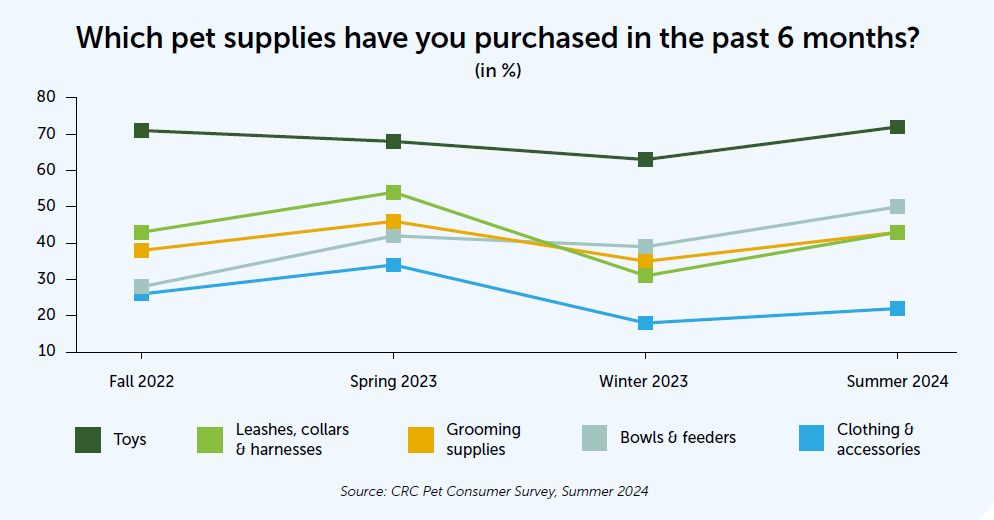

In biannual CRC surveys, US shoppers are asked what pet supplies they have bought in the past 6 months.

Findings from summer 2024 and spring 2023 indicate that these purchases are largely consistent. Toys remain the most purchased category.

Interestingly, bowls and feeders plus grooming supplies are now showing growth compared with the previous 6 months.

Opportunities for cat innovations

Although there is no true source for pet adoption metrics, the research suggests a subdued pet household environment through 2025.

As cat and dog hard goods are very much linked to adoption metrics, this influences categories like collars, leashes and beds.

There was some rebound seen in the summer 2024 survey among pet parents, compared with winter 2023 results, but with a softening in these categories compared with spring 2023.

As cat adoptions are now outpacing dog adoptions in the US, there are opportunities for leading brands to explore differentiated feline offerings such as cat tree innovations and cat beds.

Quality comes out on top

Another trend observed in the broader pet market and identified in the hard goods category, is that consumers are increasingly seeking quality when making pet purchases.

Consistent over the past 6 months, whenever pet consumers have been asked to rank product attributes in terms of importance for making a purchase, quality is at number 1. This applies to both dog and cat owners.

Quality is definitely a factor in the hard goods category, with both higher price point items and products with greater longevity doing well. The trend has been noted in traditional bricks-and-mortar purchases as well as pure-play e-commerce retail.

It holds especially true for cat toys – again an opportunity presented by recent adoption trends – and is now seen as a green shoot in the overall pet hard goods category.

Threat of copycat products

A headwind facing hard goods brands is the copycat nature of the business – particularly among pure-play e-tailers such as Amazon, Temu and even TikTok Shop.

This was identified as a theme during the SUPERZOO trade show hosted in Las Vegas in August. Brands were talking about innovation in the space being stale, and cheaper, copycat products coming onto the market.

Brands are choosing to focus their retail partnerships at bricks-and-mortar outlets in order to mitigate some of the copycat risks.

In an attempt to drive awareness of differentiation, a number of brands are starting to redefine the messaging on their packaging, so as to highlight attributes like sustainability, domestic production and durability.

DTC vs traditional retail

Another challenge for traditional hard goods brands and pet specialty retail as it functions today in the US, is the emergence of DTC brands. During the last quarter, there has been noticeable skepticism around DTC brands and the degree to which they are meaningful competitors to retailer brands.

CRC estimates the total DTC pet market in the US at $2 billion (€1.84B) as of 2024 and the market is believed to be growing, due to overall retail channel shifts.

Consumers are increasingly seeking convenience in their pet category purchases.

This trend was highlighted in recent research, when respondents were asked to indicate the importance of convenience in their pet product purchasing and marked it as 4 on a scale of 1 to 5. It is a consumer need that the DTC market obviously addresses.

To prevent more market share leaking from retail to these DTC players and to drive differentiation and innovation in their stores, pet specialty retailers are looking to bring DTC brands into bricks-and-mortar outlets.

This strategy has proven effective for DTC brands looking to scale up quickly, capitalizing on the brand awareness they’ve already built.

However, DTC brands who have a loyal shopper base have noted loss of brand ownership when moving into traditional retail, so they’re now opting instead for pure-play e-tailer partnerships or a slower progression into physical stores. Overall, the emergence of DTC brands creates awareness for branded products too, while spurring innovation across all categories.

Vital market insights

As vendors and retailers across pet retail look to drive unit sales growth in 2025, it is vital that they understand underlying market dynamics, pet shopper behavior, the appetite for innovation and the investment levels needed to grow their market share across all channels.

The hard goods category is expected to remain under pressure through the first half of next year, but there are still opportunities for retail and DTC to introduce innovative and margin-driving products.

Share this story: