The pet insurance sector in perspective

Despite the rising cost of living, the pet insurance industry continues to generate demand worldwide. What are the current trends and opportunities, and how can players in this field set themselves apart?

The global pet insurance market was estimated at around $9.4 billion (€8.6B) in 2022 and this year it is expected to jump to $10.8 billion (€9.9B), according to recent studies by Grand View Research and Beyond Market Insights. The industry is forecast to grow at a yearly rate of 16-17% until 2030, when it could reach a market value of $32.7 billion (€29.8B). Europe and North America are the strongest markets, but demand for pet insurance is also growing in other regions such as Asia Pacific.

Generational aspect

So what is driving this growth? The generational aspect is one factor, according to Lane Kent, CEO of insurance firm Independence Pet Group. “We’re seeing younger adults delaying having children and getting a dog or a cat instead. In addition, as opposed to older generations, they genuinely consider their pets part of the family, and they want to treat them as such. This includes, among other things, having a way to help cover veterinary expenses to keep their four-legged friends healthy,” he says.

Rising costs of pet care

Consumers are increasingly aware of the rising costs of pet medical care. Pet insurance company Lemonade found that, on average, American pet parents budget to spend $1,907 (€1,739) per year equivalent to 4% of their income – on pet care. Meanwhile, recent research by Credit Summit among 1,200 pet parents concluded that more than 3 out of 10 owners in the US refused to get treatment for their pets because they couldn’t afford it.

“Advances in veterinary medicine and rapidly increasing specialization are giving pet owners more options than ever before in providing life-enhancing, life-extending and life-saving treatments. However, the cost of medical services – and with that, the cost of pet ownership – is rising. Insurance provides peace of mind that financial constraints don’t have to limit care options,” Kent states.

New market entrants

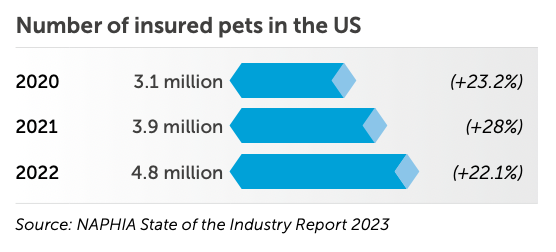

In North America, approximately 5.36 million pets were insured in 2022. According to The North American Pet Health Insurance Association (NAPHIA), this represents an increase of nearly 22%. There are already over 35 providers of pet insurance in the US, and more are entering the market all the time, says Ricky Walther, Chief Medical Officer at Pawlicy Advisor:

“We’re seeing new players come into the space with innovative ideas on how to broach the pet insurance conversation and show a value proposition to owners.”

For example, German conglomerate JAB Holding Company recently acquired a majority stake in Pumpkin, a New York-based pet insurance firm. Last year, the holding’s Pinnacle Pet Group took over German pet insurer Agila and Dutch-based Veterfina. Pet retailers are also expanding their offerings into the insurance sector, as illustrated recently by US-based Chewy and Australian Pet Circle.

Differentiation through technology

It is important for pet insurance companies to differentiate themselves in such a competitive market. Technology plays a key role in supporting value-added services, for instance, to help pet owners provide preventive care or determine how acutely a pet needs veterinary care. Additionally, many of today’s consumers expect to be able to interact with their insurance providers digitally and have direct access through apps on their mobile phones.

In this context, however, both Independence Pet Group and Pawlicy Advisor believe that existing insurance companies might not always be in the best position to serve the pet insurance market with their legacy technology platforms. This opens up possibilities for new and innovative companies. “Most of the major players have come to the space without the burden of antiquated systems and processes,” comments Kent.

“And we’ve already seen some companies adopting things like AI to help speed up the claim adjudication process,” adds Walther.

Regional differences in pet insurance adoption rates

There is a trend toward combining pet healthcare offerings with insurance, particularly in the area of preventative medicine or wellness. However, there is some uncertainty about the timeline and extent of this trend. The current focus is on educating pet owners about the benefits of insurance to increase adoption rates of pet insurance. There is certainly plenty of potential for market growth, although there are strong regional differences. In Sweden, for example, most pets are insured (95% of dogs and 69% of cats). In contrast, in the US, it is estimated that only 3% of pets are covered by an insurance plan.

“Right now, the biggest challenge I see is to get the pet insurance adoption rate up in North America in general. As the adoption rate increases, I can see lots of potential ways that insurance companies could move forward to differentiate and position themselves,” concludes Walther.

Share this story: