The changing landscape of e-commerce

Not since the Great Recession of 2008 has retail experienced such a disruptive and damaging year as 2020. There have been many changes, but not all for the worse. The pet industry seems more resilient than other sectors.

Four key impacts

Four key impacts have hit the pet industry particularly hard. First, COVID-19 puts pressure on bricks and mortar as countries experience intermittent lockdowns. Second, further integration of omnichannel where non-pet specialty brands have expanded their offerings. Third, the focus on DCM causing uncertainty and speculation about grain/grain-free formulations. And lastly, e-commerce (Zooplus, Amazon and Chewy) dominating regular pet retail.

It is not all bad news

Ultimately, consumer patterns for pet retail remained unchanged, and the necessity to stay home spurred DIY care for pets. Adoptions are up over previous years, driving new purchases of higher margin durables and creating higher value customers.

In the months following the start of the pandemic, online pet sales in the US grew by 77%, with a 28% rise in new e-commerce subscriptions. 81% of pet owners are currently more isolated and expecting e-commerce solutions. Today, e-commerce pet industry penetration is 18% and is expected to grow to 35% by 2024.

Many pet retailers have risen to the challenge, quickly reorganising and upskilling their teams to focus on much-needed improvements to realise their digital transformation strategies. Pet stores are deemed ‘essential’, but the desire for ease of purchasing leading to online demand has forced retailers to rethink priorities. This has offset some losses for retailers and helped them much improve e-commerce capabilities to make their businesses more ‘Amazon-proof’.

Global overview

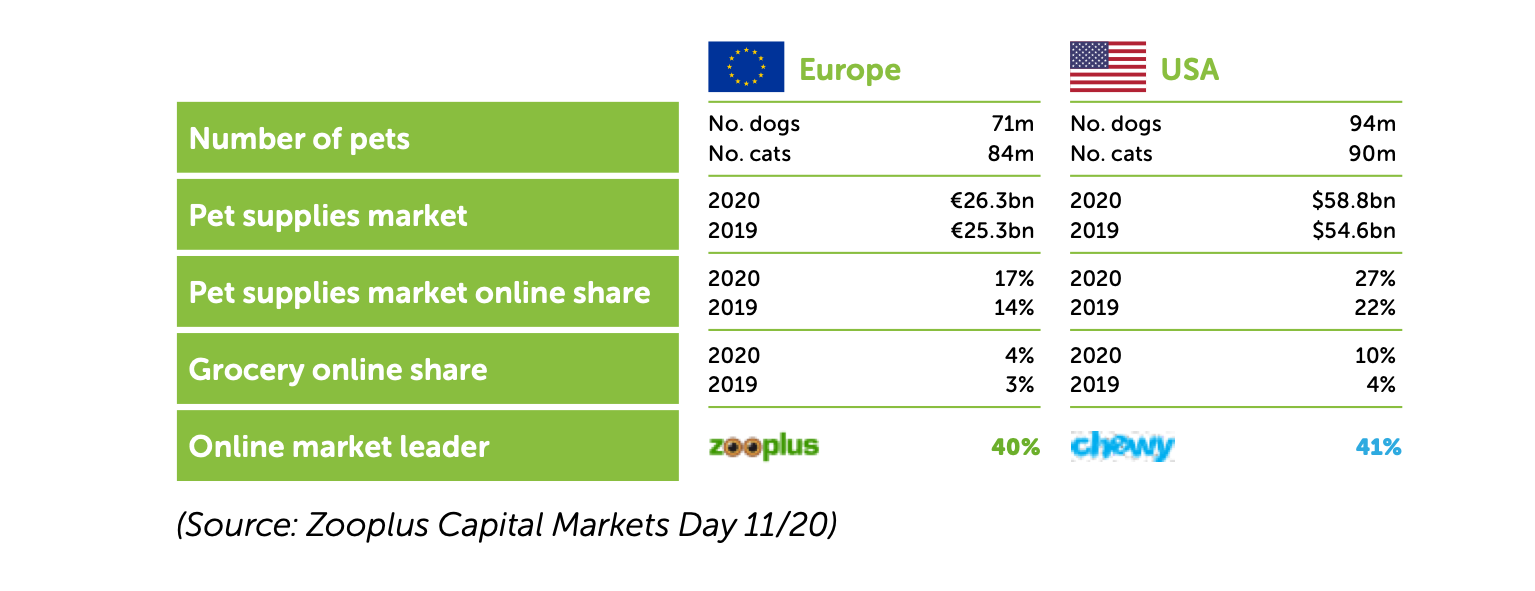

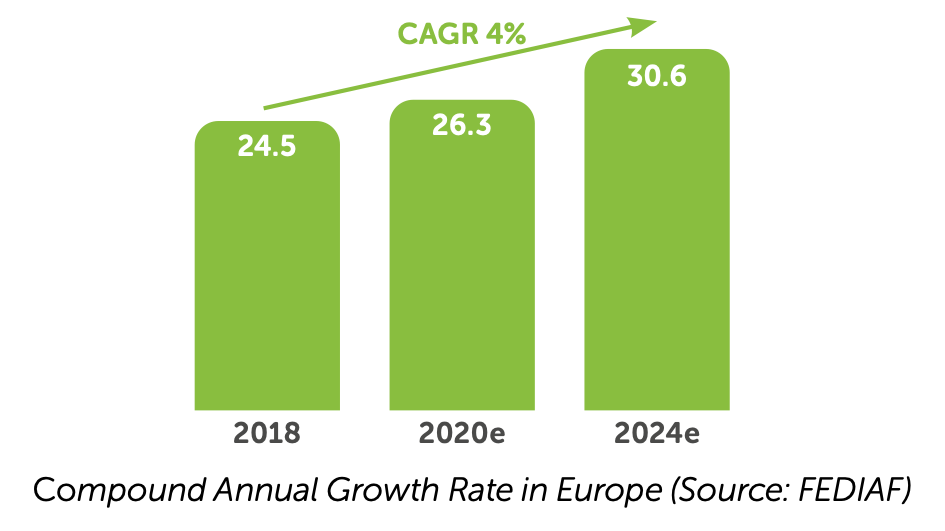

Europe now has 71 million dogs and 84 million cats (+16% and +25% compared to 2010). But while the EU pet industry is expected to grow 4% CAGR to €31 billion ($38 billion) by 2024, the US still have by far the largest pet products market, estimated at $59 billion (€49 billion) in 2020, with a 47% global share. A noticeable development is that Brazil now heads a second tier of markets worth more than $1 billion (€823 million).

Key drivers of the growth in sales include the trend towards specialised nutrition and continued premiumisation, as 90% of pet owners now consider their pet a part of their family. Both Packaged Facts and Euromonitor expect healthy growth for the pet care market in 2021, registering 7.6% growth, with pet food increasing 5.5%.

Online players well positioned for growth

Chewy, the US’s largest online pet retailer, announced guidance of $6.8 billion (€5.6 billion) in 2020 revenues (+40% YOY) and break-even EBITDA for the first time.

Zooplus has continued to steal market share from offline businesses and recently reported record sales growth. With more than 4.9 million active repeat customers, 77% of whom are female, their sales per customer is now €380 ($467).

While change and disruption are constants, agile adoption to dynamic needs should remain a key priority for all pet retailers and manufacturers in 2021.

Share this story: