Macroeconomic pulse (I): consumer spending and retail activity across major economies

Household income and consumption trends continue to underpin economic activity.

Some of the world’s largest economies have been showing positive economic results, with household consumption, retail and services sales growing between the end of 2025 and the beginning of 2026.

While indicators point to a favorable scenario for business, due to expanding demand, geopolitical tensions stemming from the ongoing conflict in the Middle East threaten to put the economy in check.

GlobalPETS analyzes activity indicators in the United States, the United Kingdom, the European Union and China.

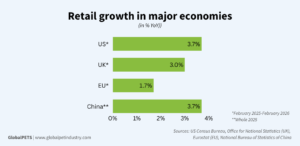

Retail activity

In Great Britain, retail sales rose by 0.7% in the 3 months to February 2026, compared with the 3 months to November 2025, according to data from the Office for National Statistics (ONS). Compared with last year, sales volumes increased by 3%, marking the best quarter since February 2023.

The growth was driven by “non-store retailers” – that is, mainly online retailers but also including street stalls and markets. This segment registered a 2.7% increase in sales during the quarter, with a peak in January. While food and household goods stores improved slightly, department stores, textiles and footwear registered declines.

The US also had a positive result: a 3.7% annual uptick in retail and food service sales in February, reaching $738.4 billion (€630B), according to data from the US Census Bureau.

Just like in the UK, nonstore retailers’ revenue posted stronger growth, up 7.5% from last year. Miscellaneous store retailers, which include pet and pet supply stores, posted an 11.6% yearly growth rate, the strongest result per category.

The European Union and the eurozone also registered year-over-year (YoY) growth in February, but at a slower pace: 1.7% in both cases. Although retail sales volume decreased in February compared to the peak at the end of 2025, the index has been on an upward trajectory since 2021.

The 3 main segments into which Eurostat divides the data showed growth, although in different dimensions: food, beverages and tobacco increased by 0.9%, non-food products grew by 2.3% and fuel for vehicles in specialized stores rose by 1.6%.

China had the same YoY increase rate as the US, at 3.7%, reaching ¥50.1 trillion ($7.3T/€6.3T) in retail sales of consumer goods in 2025. “The sales of basic living goods and certain upgraded goods witnessed good momentum of growth,” the Chinese National Bureau of Statistics analyzes.

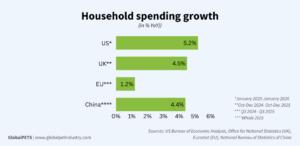

Household spending

In the US, personal consumption expenditures increased by 0.4% in January, according to the US Bureau of Economic Analysis, following a 0.4% increase in personal income in that month. Expenses reached $21.5 trillion (€18.4T) in the month, an annual jump of 5.2%.

With income strengthened by higher salaries from the private sector and more social security benefits, Americans spent more on services than on goods, with increases driven by healthcare, housing and utilities, and financial services and insurance.

Purchases of goods were driven by food and beverages, recreational goods and vehicles, and durable household furniture and equipment.

The UK releases consumer trends quarterly. From October to December 2025, household spending grew by 0.4% YoY. For the whole of 2025, the YoY uptick was 4.5% at current prices, with total expenditure approaching £1.8 trillion ($2.4T/€2T). However, when seasonally adjusted, the growth falls to 0.8%.

According to the ONS, Britons spent 2.1% more on recreational items and equipment, gardens and pets – £51.2 billion ($68.7B/€79B) – but less 0.7% in pets and related products – to £11.9 billion ($16B/€13.7B) – and 2.7% in veterinary and other services for pets – to £6.5 billion ($8.7B/€7.5B).

The most recent data available for the European Union refers to the third quarter of 2025. During this period, household consumption per capita increased by 1.2% YoY. Household income per capita also expanded 1.2% YoY, driven by higher salaries and social transfers.

Both spending and income have been steadily increasing since 2017 (with the exception of the declines during the COVID-19 pandemic).

In China, per capita consumption expenditure increased by 4.4% YoY in 2025, with stronger growth in rural areas than in urban areas. By segment, growth was boosted by miscellaneous goods and services (11.2%), education, culture and recreation (9.4%), transportation and telecommunication (8.3%), and household facilities (7.7%).

As in other countries, China also saw an increase in nationwide per capita disposable income

(5% YoY) in 2025.

Opportunities tempered by global instability

Looking ahead, the persistence of this growth cycle will depend on the delicate balance between economic fundamentals and external shocks. Higher incomes and evolving consumption patterns – particularly the continued shift toward services and digital retail – offer a supportive backdrop for businesses operating across sectors, including pet care.

However, with geopolitical instability still unfolding, the risk of sudden disruptions cannot be overlooked. For industry players, agility will be essential, not only to capture demand in the current environment, but also to navigate potential volatility in the months ahead.

Share this story:

One click prioritizes GlobalPETS in your search results and AI answers.