Deal or no deal? Pet industry M&A in 2026

Falling interest rates and a booming financial market may increase the appetite for deals, but tight finances and uncertainty make companies in the sector cautious.

It’s still early to talk about a full recovery in 2026, experts say, but there could be some movement in the acquisitions landscape. Although fiscal activity cooled recently due to high interest rates and inflation, a positive push driven by industry resilience and promising segments is anticipated.

Improved macroeconomic conditions

Last year was comparatively quiet in comparison with prior peak years, but this was mainly due to a normalization following the pandemic boom, says Oleksandr Pidlubnyy, Senior Portfolio Manager of Thematic Equities at Allianz Global Investors, which manages the Allianz Pet and Animal Wellbeing fund.

“As growth normalized, companies have also faced headwinds from higher inflation, weaker consumer sentiment, and rising input and labor costs, particularly in veterinary services and specialty care such as advanced veterinary treatments,” Pidlubnyy tells PETS International. But despite the recent challenges, the industry is cautiously optimistic.

“Both institutional investors and operating companies are poised to benefi t from easing macroeconomic conditions,” Aarti Kapoor, Managing Director in Consumer and Retail Investment Banking at investment bank Cascadia Capital, says. Beyond decreasing interest rates, Goldman Sachs forecasts moderate inflation and sturdy growth for major economies in 2026.

Searching for synergies

Experts talking to PETS International agree that strategic buyers – firms purchasing others to grow – who are already active in the pet care space are the most likely to fuel activity this year, and say they will be seeking either revenue or cost synergies. This means that companies will look for complementary businesses that will help them save money or improve gains.

But for Anna Skaya, General Partner at the independent pet-focused venture capital fund AniVC, strategic buyers “are doing smaller deals and paying attention to profitability and very specifi c capabilities or brands, especially where there is a clear opportunity”.

In a recent analysis of the pet sector in the US, Cascadia Capital found an increase of strategic acquisitions in the past 10 years across all sectors in the country, as they went from representing 17% of deals in 2015 to 32% in the first nine months of 2025.

This happens because organic growth becomes challenging to achieve as companies mature, Kapoor says. “The ‘buy’ versus ‘build’ strategy has been particularly relevant with target companies offering incremental capabilities – whether new product categories, form factors, end markets or other characteristics – where strategics would otherwise need to develop those capabilities internally,” she explains.

Europe vs the US

In the US, institutional investors such as private equity firms have a lower participation in acquisitions in general, approximately 11%, but they have “meaningful dry powder”, Kapoor says, i.e. cash reserves or liquid assets ready to be invested.

She goes on to say that these investors are expecting to benefit from lower interest rates to finance deals.

A recent example was the purchase, last June, of UK premium pet food business MPM Products by private markets investment firm Partners Group.

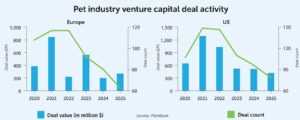

Global pet industry venture capital activity in 2025 reached approximately $900 million (€755M), with 262 deals recorded by the private market data company PitchBook. The amount that changed hands in Europe was $267.3 million (€226M), representing 62 deals. The US market registered more intense activity, with 78 deals totaling $411.2 million (€344M).

The glowing health segment

The experts also agree that health is the most attractive segment within the pet industry. For Skaya from AniVC, it is diagnostics, longevity and preventative care that stand out. “Longevity in particular feels like the clearest expression of how much people are humanizing their pets,” she says, adding that a combination of real science – or data with strong consumer branding – is also a good target for early investors.

For Tom Elliott, Managing Director of Consumer Goods Investments at Capstone Partners, veterinary care in general is a segment with several large consolidators, i.e. large companies interested in buying small ones, such as North American chain VCA Animal Hospitals, owned by Mars, and Texas-based National Veterinary Associates, owned by JAB Holding Company.

Elliott also points to insurance as a promising field. According to market research company DataM Intelligence, US-based Embrace Pet Insurance completed the acquisition of Healthy Paws’ policy portfolio in 2025. In Europe, the French group Santévet acquired a majority stake in the UK-based pet health insurance provider Tedaisy in July.

Investor appetite in consumables

There are three other categories with the potential to attract investors. One of them is consumables, with Cascadia Capital estimating that several assets in this segment that received investments or were acquired in 2020 can re-enter and test the market, such as the premium and sustainable pet food manufacturers BrightPet, Nulo, Open Farm and Primal.

Online retail is another area of interest. “Consumers increasingly value convenience, especially for repeat purchases and more commoditized products,” says Pidlubnyy. And at the end of December, French pet e-commerce player Zoomalia was acquired by Holding Nicole, the parent company of the JMT Le Royaume des Animaux retail chain as “a strategic approach to the complementation of business models”, according to Fanny de Valon, Marketing Director of JMT Réseau.

Skaya believes that companies that “elevate the pet and pet parent experience”, such as US companies Lil Luv Dog (fancy and sustainable grooming products), DOG PPL (a canine social club with park, café, bar and lounge) and RetrievAir (which provides a “pet-first” flying experience), are other interesting candidates for investment.

Threats to successful deals

One of the main obstacles for investments and acquisitions this year is the weak performance of some companies, especially on the product side, says Elliott. Due to the drop in consumption, he explains, these firms are waiting for better financial conditions to secure better deals. “Nobody wants to sell when their sales are lower,” he says.

As a backdrop, a report published by consulting firm McKinsey in December 2025 points out that “consumer sentiment had dropped considerably compared with the beginning of the year” and “discretionary spending intentions softened, with consumers signaling plans to pull back across most non-essential categories”.

According to Skaya, weak differentiation and high customer acquisition cost continue to be common reasons why companies struggle. Experts believe that a potential risk is overpaying for acquisitions. “In strong equity markets, valuations can become elevated, increasing the risk that buyers pay more than a company’s intrinsic value,” says Pidlubnyy.

Positive indications

The equity market had one of its best years in 2025, pushed by AI and tech stocks. Stocks are at an all-time high. The S&P 500 is currently trading at 30.5x earnings and 3.9x revenues, according to an analysis by the Seeking Alpha platform for investors, published in October 2025.

In terms of deal payment, there are differences within the pet sector. Analyzing a database of more than 215 transactions since 2010 with disclosed or proprietary multiples, Cascadia Capital’s report points out that, in the past 15 years, animal health deals have reached a mean multiple of 19.7 times the EBITDA profitability measure, followed by veterinary (17.3x), consumables (12.6x), retail (10.6x) and product (8.8x).

Could IPO surge in 2026?

Despite the positive performance of capital markets, experts are still hesitant about an uptick in Initial Public Offerings (IPOs) within the pet sector. Pidlubnyy recognizes that the environment could improve over the coming years and sees the pet care industry as structurally attractive, with growth rates exceeding GDP in most developed and emerging markets.

Along the same lines, Elliott says that private equity owned companies looking for an exit could consider an IPO, and here too sees health as the most probable candidate to lead it. 2025 did give some indications of what’s to come.

In July, the pet biotechnology company Akston Biosciences fi led a form to the US Securities and Exchange Commission to launch an IPO. The firm focuses on biopharmaceutical products for cats, dogs and other companion animals, and has developed a GLP-1 treatment targeting feline obesity. Media outlets reported that the Indian company Zenex Animal Health was also exploring this possibility at the end of last year.

In Australia, the market expects an IPO from Greencross, a retail and veterinary chain. According to local media, TPG Capital, the US private equity firm that owns it, plans to raise about A$700 million ($460M/€420M) in this initial offering, aiming for a valuation of A$4 billion ($2.6B/€2.4B). An IPO is being considered by the firm as an exit strategy after unsuccessful attempts to sell the company in 2023.

What funds are looking for

As a fund, AniVC is looking for real proof of demand and product market fit, strong unit economics and a path to profitability early on, Skaya says. In its role as early-stage investor, it values “founders who deeply understand the customer” as well. According to her, AI is now making it “easier than ever to put together a pitch deck, so the real work is separating companies that can scale within a venture model from ideas that still need time”.

The Allianz Pet and Animal Wellbeing Fund focuses on long-term growth opportunities arising from how pets are cared for. As Pidlubnyy says: “In an environment marked by economic and geopolitical uncertainty, this theme remains highly relevant, as spending on animal health and care has historically proven less cyclical than broader discretionary consumption.”

In this way, pet-related business as a whole, with its combination of strong fundamentals and valuation levels, stands out as a long-term viable option.

Share this story: