How pet food fared in Black Friday week

This annual sales event is also on the pet industry calendar, with many retailers opting for strong promotional activity. PETS International compares the week’s sales in 2023 with the same period in 2022.

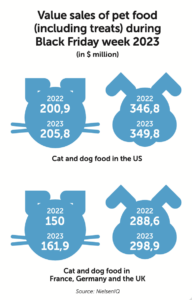

Originating in the US, Black Friday has become an increasingly important sales opportunity around the world. Data for food and treats in the US, France, the UK and Germany shows which sales channels and product categories were the late November winners and which lagged behind.

US grocery stores beat pet specialists

During the week of Black Friday 2023, Nielsen value sales data for the whole cat and dog food category in US pet specialists and e-commerce showed cat food posting a modest 2% growth, while dog food grew by 1%.

Retail sales at grocery stores gave a more positive performance. Cat food increased by 8% that week, and dog food by 4%. In this channel, total pet food reached $460.4 million (€425M), representing 5% growth. This is still below 2022 performance, when total value sales grew by 17%.

Effects of higher prices

In 2023, the pet industry wasn’t immune to the inflation spikes experienced globally and prices soared in the US market. This put many pet-owning households under increasing pressure. On average, prices at pet specialists increased by 20% for cat food and 31% for dog food. This had an impact on sales, making consumers more price-conscious and causing volumes to suffer.

From an overall category perspective, volume sales for cat food posted an 8% decline and dog volumes shrank by 10%, a trend that continues from previous years. Nevertheless, analyzing per household value expenditure, the scenario is quite different for dog and cat owners. Cat owners increased their spending across all categories, whereas dog owners remained more cautious.

Wet cat food wins at specialty stores

Posting 7% value growth, wet cat food was the best- performing category among pet specialists in the US. That was followed by cat treats, which grew by 3%. Although volume per household declined in both categories, -13% for wet food and -22% for cat treats, wet food sales reached $101.6 million (€93.8M) and cat treats amounted to $15.7 million (€14.5M). This shows that pet parents will go to great lengths to pamper their pets, as well as how important food quality and variety are for cat owners.

Other types of cat food

A category where price seemed to have had a clear impact on consumer choices is newer types of cat food, such as fresh, frozen, freeze-dried and dehydrated. Value sales for this declined by 7% at pet specialists and, with prices having risen by 37% in a year, cat owners seemed to have shifted to more affordable categories as volume sales dropped by 32%. This is in contrast with category performance at grocery stores, where sales grew by 15%. Dry cat food value sales in this channel also rose by 11%, outperforming wet cat food, which grew by just 5%.

Differences in dog food

The picture differs greatly when it comes to dog owners. Value sales increased across the whole dog category, except for dry food. But, similarly to cat food, volume sales declined across all but one category. Dog treats suffered the steepest decline, with volume sales dipping 33% and unit prices rising 55%.

In value terms, it was the newer types of dog food that were clear winners. Experiencing a 63% value rise, it was the only dog food category where value sales were also coupled with a staggering 43% volume sales rise – although departing from a lower base. Sales of this product category at pet specialists amounted to $28 million (€25.8M).

Sales per household increased by 20%, as new consumers were drawn to this format. Mass-market value sales experienced a similar performance, with the category outperforming all others. Value sales reached $18 million (€16.6M) from $13.7 million (€12.6M) in the previous period, a 31% increase.

Wet dog food was the second best-performing category, as value sales increased by 6%. There seems to be a renewed demand for wet food, despite prices increasing by 24%. Looking at dollars spent per household, nothing could beat the appeal of dry food, with households spending $30 (€28).

Cat food outperforms dog food in France

Cat food value sales at pet specialists reached €39.5 million ($42.8M), with 6% growth. The category was even more dynamic at grocery stores, where sales amounted to €37.6 million ($40.7M) and posted a 10% increase. With cat value sales in mass-market representing double those of dog food, this increase is no small feat for the industry. Owners seem to have spared no expense to pamper their cats, and this was seen in both channels.

Wet multi-serve for cats does well

At specialists, wet multi-serve cat food posted an impressive 29% value sales increase and treats rose by 15%. Rising prices didn’t keep consumers away – some of the biggest price hikes occurred in these 2 categories. Wet multi-serve prices rose by 25% and cat treats by 17%. Wet multi-serve cat food also performed better than other categories in mass-market, as sales grew by 21% despite a 16% price increase.

Dog sector sales disappoint

At pet specialists, dog food sales reached €23.6 million ($25.6M), a disappointing 14% decline. Dry dog food was one of the main category losers, as value sales went down by 22%. The category performed better in mass-market, where sales flatlined and total dog food sales stood at €17.1 million ($18.5M), representing a mere 1% increase.

UK cat owners prefer grocery stores

The pet industry in the UK has been faced with several challenges recently. From the inflationary pressures across most of 2023 to the supply chain challenges related to Brexit, pet manufacturers have had a lot to contend with.

Cat food value sales experienced a 1% decrease at pet specialists but grew by 7% in mass-market, where sales were £3.2 million (€3.7M/$4.1M) – driven by the good performance of both dry and wet cat food. Wet food sales at pet specialists, at £23.3 million (€27.3M/$29.6M), did help to stave off a general decline there, with total cat food reaching £33.9 million (€39.7M/$43M), despite a 13% drop in dry food and treats.

Dog treats and multi-serve keep up

At the total category level, value growth was flat for dog food at grocery retailers, but up 2% at pet specialists. Good performance by dog treats at specialists meant that dog value sales reached £39.6 million (€46.4M/$50.3M). Treats were one of the largest categories at £14.5 million (€17M/$18.4M), posting 7% growth. Wet multi-serve was the best- performing category, with 15% value sales growth it was the only one to also increase volume sales, by 7%.

German pet owners unfazed by price hikes

The trends in the German pet food market were very different to the other countries. Value sales for cat food grew by 11% during Black Friday week, reaching €36.9 million ($40M) in mass-market. At pet specialists – including e-commerce – value sales for cat food amounted to €39.6 million ($42.9M), representing 3% value growth.

While this was already good news for the industry, dog food sales were even more successful. Their value sales reached €33 million ($35.8M) at German specialists, an impressive 21% growth, and €18.7 million ($20.3M) at grocery and pet stores – 6% growth.

Impressive dry dog food sales

At pet specialists, dry dog food was particularly appealing to German consumers, posting a staggering 64% value growth, even in the face of prices rising by 15% since the previous year. Wet multi-serve was also popular among dog owners, with sales increasing by 33% as prices rose by 31%.

Satisfactory cat food sales

Cat food value sales at grocery and pet stores posted good growth, with dry food rising by 17% and wet food by 9%. Wet food sales account for 80% of total cat food. Cat care and treats also performed well, with sales reaching €6.7 million ($7.3M) – 13% growth. At specialists, cat dry food sales for that week amounted to €8 million ($8.7M) – 21% growth – and wet food €25.3 million ($27.4M) – a 3% decline.

All sales data given in this article refer to the week of 24 November 2023. All percentages compare the data with sales during the same week in 2022.

Share this story: