Keeping pace with UK spending trends

Pet food persists as an appealing category for retailers and investors alike, but value remains king in the bid to attract and retain British shoppers.

According to new consumer research, value reigns supreme in the UK pet food category, but spending is expected to rise and loyalty remains strong. What can brands, manufacturers and retailers do to improve their chances of success?

The watchword is value

Data from PwC Strategy& primary consumer research shows that around 15% of pet owners adjusted their buying habits during the cost-of-living crisis in the UK. In 2022-23, 56% of these consumers purchased pet food in bulk to save money, while 47% sought discounted products.

These habits have proven sticky. Even after 2023 47% continue to buy in bulk and 34% still take advantage of discounts. This indicates that ‘value is king’; pet parents are increasingly discerning about how they allocate spend within the category.

Pet food spend expected to rise

Nevertheless, purchasing of pet food continues to demonstrate resilience relative to many other consumer goods categories, despite the prolonged economic uncertainty in the UK.

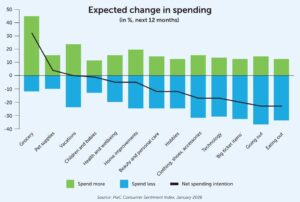

The statistics continue to show that pet food remains an area of protected spend – ahead of vacations and babies. On balance, British pet owners expect to increase expenditure over the next 12 months, even as spending intentions remain constrained elsewhere.

When asked about their top purchase criteria for pet food, owners placed “my pet enjoys the taste” first (78%), making it the most important factor across the board. “High quality” came in second (59%), followed closely by “reasonable price” (55%). Taste was slightly more decisive for cat owners than dog owners, but it remains a key driver for all pet parents.

Private label vs branded products

The recent inflationary cycle has reshaped the competitive dynamics between branded pet food and retailers’ own brands. Private label pet food gained market share in 2023, rising to 14-15%. This was largely driven by mid-market and value shoppers trading down from branded products amid rising cost pressures. Growth was also supported by increased shopping at discount retailers.

Today, private label products account for around 13% of pet food value, which is broadly in line with long-term trends. However, while branded products have regained momentum as macroeconomic conditions stabilize, private label products continue to evolve, with improvements in quality, formulation and packaging.

As a result, branded manufacturers must justify premiums through demonstrable benefits, such as functional nutrition, ingredient transparency or veterinary endorsement. Meanwhile, retailers must carefully manage assortments to balance value perception with margin and brand equity.

Embedded multichannel behavior

When it comes to purchasing channels, pet food sales in the UK remain dominated by grocery stores (around 40%) and pet specialty retailers (around 25%). However, online channels have grown significantly over the past five years, in a way that sets pet food apart from other consumer categories.

Online penetration jumped during Covid, rising from roughly 18% of sales in 2019 to 27% in 2021. Unlike many other sectors, which saw online sales decline again after the pandemic, pet food has continued to shift online. Today, it captures about 32% of the market.

Most UK pet parents now adopt a multichannel approach, with 53% of cat owners and 50% of dog owners shopping both online and in-store, according to PwC Strategy&’s latest data.

Growth in DTC and subscriptions

Direct to consumer (DTC) remains a key channel for some brands selling in the UK, particularly those targeting dog owners. This highlights the importance of pet food brands having a clear strategy across multiple channels, defining the role of each channel both strategically and at every stage of the customer journey.

From an investor perspective, DTC metrics are scrutinized closely. Detailed diligence on customer cohorts, and the ratio of the company’s customer lifetime value to its acquisition cost (LTV/CAC ratio), form a critical part of assessing any business.

Moreover, the research indicates that subscription models are likely to stay popular among UK pet parents. This popularity is driven by convenience (68% of users), good quality (58%) and high-quality food (48%). Current subscribers tend to be relatively affluent, with 50% reporting household incomes of £150,000+ (€173,609/$199,163), younger (around 65% are under 54), and more often dog owners.

Loyalty and barriers to switching

Despite greater choice and growing channel fragmentation, brand loyalty in UK pet food repertoire of brands – up to around 10 in the case of cat owners – over a 12-month period. This reflects regular behavior reinforced by trust, and the perceived risk of switching. Loyalty is strongest for brands that meet multiple needs across life stages or functional requirements.

Trialing remains crucial, but this can be challenging – especially among cat owners. According to the research, a cat’s taste preferences are the biggest barrier to switching. Nevertheless, some owners indicate they may consider trying a new product if they are offered a meaningful discount. This underscores the importance of product distribution, visibility and clear communication in driving growth.

Looking to the future

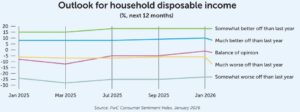

Having tracked the sentiment of around 2,000 nationally representative consumers over the past 18 years, PwC Strategy& is able to draw meaningful conclusions about future outlook. After some nervousness ahead of November’s UK Budget, British consumers are now feeling relatively positive about the future. The sentiment tracker rose to around 0 in January 2026, well above the long-term average of approximately -15.

The research findings outlined above point to a UK pet food sector that remains structurally resilient yet competitive. While overall market growth is expected to continue, value creation will hinge on execution rather than demand alone.

The brands, manufacturers and retailers that succeed will be those that clearly articulate value, operate effectively across channels, and continue to earn consumer trust in a category where purchasing decisions are closely tied to perceptions of care and responsibility.

Share this story: