New channels and humanisation dictate Canadian petcare industry

Petcare stands out as a dynamic industry in Canada as pet ownership, particularly of dogs and cats, consistently grows.

Three big changes

Canada’s petcare industry is the twelfth largest globally and in the last five years it grew an impressive 21% in retail sales. This was more than twice the rate of most other Canadian consumer packaged goods (CPG) industries, with continued growth on the horizon.

Despite this growth, major trends are disrupting the industry and have the potential to transform petcare in Canada. Three trends, in particular, should be watched closely in 2019.

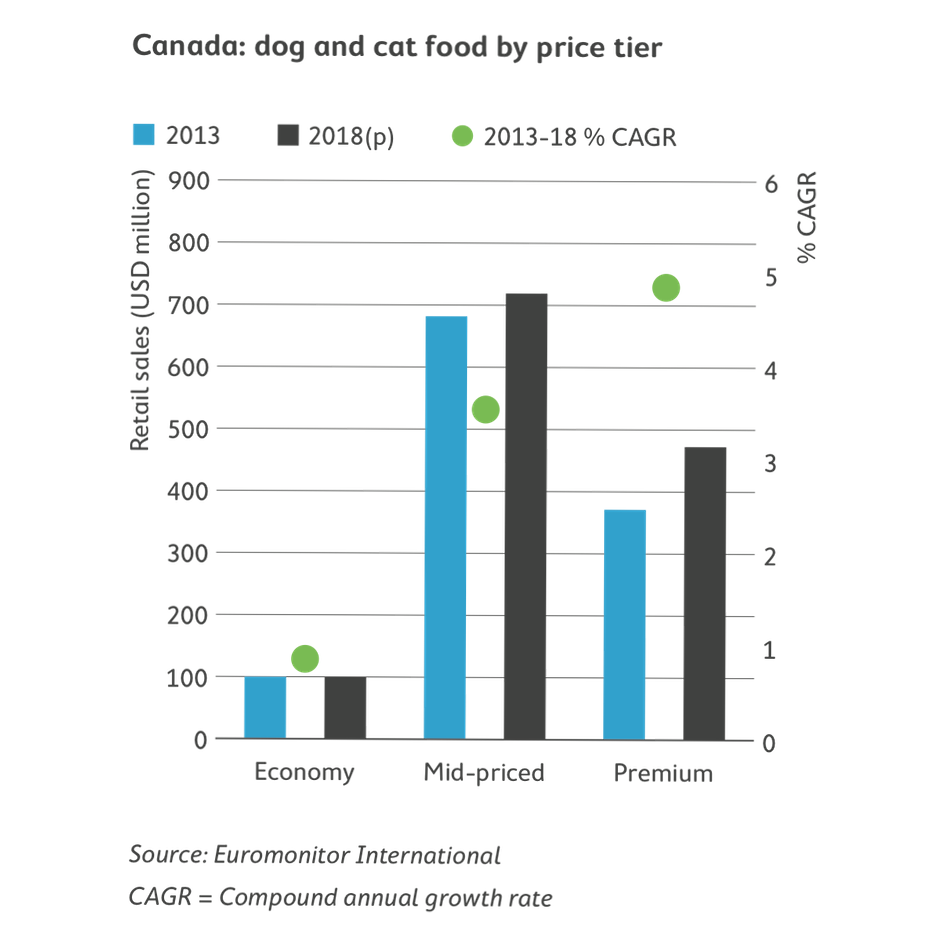

Wanting only the best

Humanisation and premiumisation will continue to shape the Canadian petcare market and these trends are expected to intensify. Consumers now view their pets more as companions and family members, bolstering demand for premium products traditionally geared toward humans. Food products touting alternative proteins, natural qualities and special dietary attributes are expected to continue to steal market share from economy brands.

Accessories and even dietary supplements for pets are projected to achieve strong growth, along with smart technology products. More and more pet owners are purchasing GPS and activity trackers, health monitors, and food and treat dispensers.

Channel identities redefined

The rise of speciality foods and the demand for premium offerings could indirectly impact channel distribution. Traditionally, the industry has been largely segmented into two distribution groups with distinct brand offerings. Mass channels – which include supermarkets – warehouse clubs and other mass merchandisers have largely been geared toward selling economy and mid-priced brands that offer basic nutritional attributes. Conversely, speciality channels such as pet shops and veterinary clinics have prioritised premium brands and therapeutic brands.

Channel identity has historically been vital to the industry, with many consumers associating speciality channels with quality. As demand for premium items has soared, so has the speciality channel, which grew by 9% in 2018. But as consumers continue to look for speciality products while shopping across channels, the likelihood of disruption to the traditional divide between these channels grows. This could cause speciality brands to proliferate in mass channels and vice versa.

Channel identity has historically been vital to the industry, with many consumers associating speciality channels with quality. As demand for premium items has soared, so has the speciality channel, which grew by 9% in 2018. But as consumers continue to look for speciality products while shopping across channels, the likelihood of disruption to the traditional divide between these channels grows. This could cause speciality brands to proliferate in mass channels and vice versa.

In the US, this traditional divide is already less distinct. Mass channels are now seeing a slight increase in growth, as a result of strong sales for premium items that were previously reserved for speciality channels. It is a trend that could well be an indication for the future for Canada too.

Explosive growth of e-commerce

Transformations within petcare are most powerfully seen in the rapid ascendance of e-commerce. As connectivity grows, and millennials in particular prioritise convenience, e-commerce has seen explosive growth across many CPG industries. While still premature in many food categories, petcare internet retailing in Canada has surged, growing 277% since 2013 to account for 2.6% of all petcare sales. Much of this growth can be attributed to online giants like Amazon expanding in Canada, as well as popular delivery subscription services providing the ultimate convenience.

However, brick-and-mortar stores are also incorporating e-commerce delivery and popular in- store pickup options. As more retailers make these options available, and more consumers shop online, petcare represents one of the ripest industries for e-commerce to mature in 2019.

Detailed report

Despite strong projected growth in the industry in the immediate future, these three trends will create upheavals as they shift and change traditional dynamics. A report on petcare in Canada on the Euromonitor website gives more details on how changing purchasing behaviour and new technology are likely to cause continued disruption in the growing Canadian petcare market throughout 2019.