US pet parents remain loyal to their brands

Despite concern about the money in their wallets, the majority of American consumers aren’t willing to make concessions when it comes to buying products and services for their pets.

While the broader consumer market in the US faces trade-down pressure as consumers react to the rising cost of living, the pet industry stands out for its resilience. Surveys indicate that the bond between pets and their owners is key to this.

Loyalty drives pet consumer commitment

The strong customer loyalty seen in pet categories is providing insulation from the significant trading down found in other consumer categories.

PricewaterhouseCoopers (PwC) proprietary credit card data indicates that pet services – including grooming, walking, boarding and training – have continued to grow, with a 3% year-over-year (YoY) increase in spending.

But pet product purchases, on food or toys for example, have declined by 3% YoY, pointing to some price sensitivity.

The resilience of the sector overall is also noticeable in pet parents’ continuing brand loyalty, with 57% of them considering themselves “loyal” or “very loyal” to their pet service provider.

More than half (56%) of the 1,000 pet owners in a PwC survey undertaken in March this year of 4,000 consumers feel a connection to their pet product brands, and this reduces the risk of significant trading down.

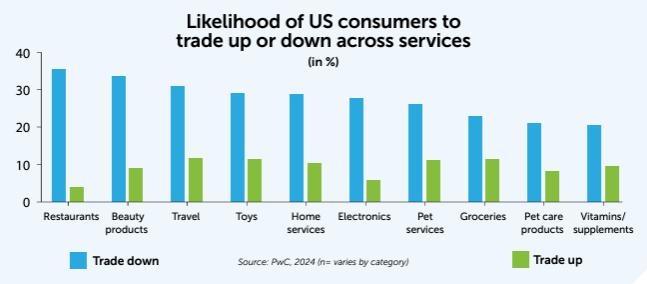

Less likely to trade down

US consumers indicate a lower likelihood to trade down in both pet products and services when compared with other categories.

This is the lowest for consumers using pet services compared with all other service categories, and the third lowest for pet products among all product categories, trailing only groceries and vitamins.

Nevertheless, price remains a critical factor for those considering switching brands, particularly among pet products.

Although the majority of consumers (68%) expect not to switch brands, of those that do plan to switch, price is an overwhelming factor, with around 5 out of 10 respondents noting it as a primary reason.

Vet prices don’t deter pet parents

Price pressure is not just evident in pet products but has also been experienced by the consumer with regard to vet services.

According to the PwC survey, 70% of pet parents visited a vet in the past year. More than 9 out of 10 of them believe there had been price increases compared to the previous year.

PwC analysis confirms that vets have raised their prices by an average of around 10% over the past year alone.

However, high pricing is unlikely to deter pet parents from getting the care they need for their pets, as 62% of pet owners state that they would be willing to go through financial hardship for their pet’s care.

Pet insurance appears to be well positioned to benefit from the rising costs of vet services, the overall pressure on the consumer wallet and the importance of pets to their owners.

Currently, only 12% of US consumers surveyed have pet insurance, but 19% plan to purchase it in the near future.

Millennials and Gen Z are the most likely to buy pet insurance (35% of Gen Z and 30% of millennials).

This creates significant tailwinds for the industry, as younger generations are also much more likely with adopt a pet in the next 6 months (31%) compared to older generations (12%).

Pet ownership returning to pre-pandemic levels

According to the 2024 Dog and Cat Report published by the American Pet Products Association (APPA), pet ownership in the US has stabilized after the pandemic surge.

It is believed that 82 million US households (63%) own a pet. In 2010, 62% of US households had at least 1 pet, some 73 million homes.

Between 2014 and 2018, pet ownership had risen to the higher levels of 65-68%, and this peaked during the pandemic year of 2020, with 7 out of 10 US households owning a pet.

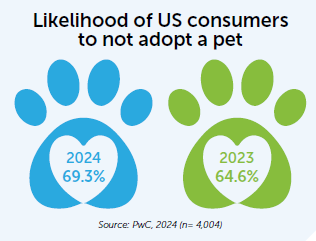

PwC forecasts another 2-3 years for pet adoption growth to return to pre-pandemic rates, as consumer hesitancy to adopt new pets persists. The recent survey suggests that 70% of consumers are unlikely to adopt a new pet in the next 6 months, while 11% are considering giving up a pet.

Interestingly, while Gen Z and millennials appear to be the most likely to adopt a new pet, they are also the most likely to give up a pet in the near future. Those who live in an urban area are significantly more likely to give up a pet in the next 6 months, with 18% of urban respondents considering doing so.

Consumer-reported unwillingness to adopt new pets remains at a high level, even as more time has passed since the pandemic, further indicating that the category will require additional time for full recovery.

Share this story:

One click prioritizes GlobalPETS in your search results and AI answers.