Zooming in on key pet industry deals in 2025

With notable activity across the sector, PETS International analyzes 50 investments that took place from January to September.

Despite a macroeconomic environment affected by uncertainty, the imposition of US tariffs, geopolitical tensions and rising inflation, the pet market has seen positive movement in mergers and acquisitions (M&A) so far this year. Venture capital and private equity firms have remained active, and have strengthened negotiations alongside strategic acquisitions, both vertical and horizontal.

Against the tide

The activity level goes against the general market trend, as the first half of the year was marked by a 9% drop in deal volume but a 15% increase in values, according to the PwC 2025 mid-year outlook.

Among the deals assessed by PETS International, only 4 had their values disclosed. Only 1 achieved $1.5 billion (€1.3B), and the other 3 ranged from $13 million (€11M) to $62 million (€53M). The analysis shows a fragmented scenario in terms of size, with a bigger presence of smaller transactions for geographic or portfolio expansion.

Pet food fundamentals

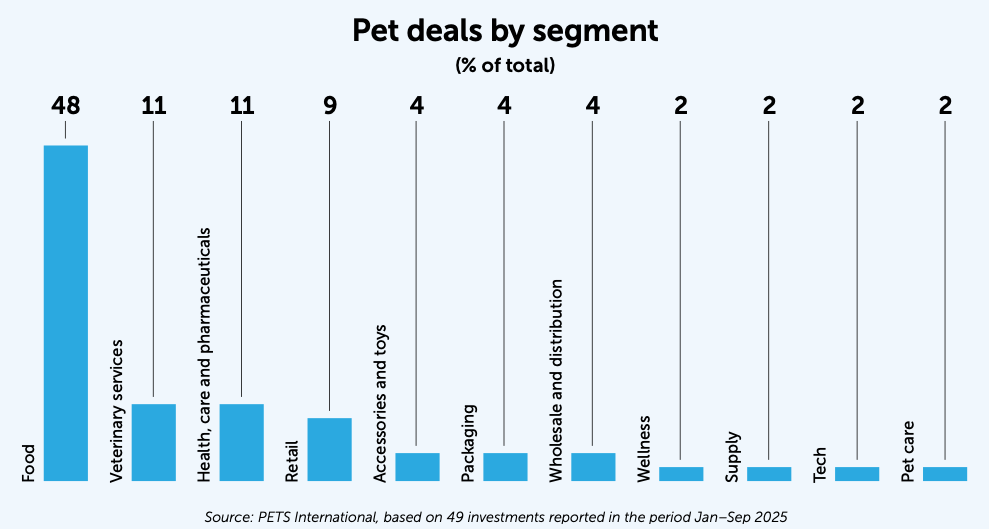

The analysis concludes that almost half of the main M&A deals in the first 9 months of the year covered the pet food market, including nutrition and treats.

As many as 8 of them involved The Nutriment Company. This Sweden-based firm has acquired strategic and family-owned players in the UK, Germany, Spain and France, aiming to profit from the rising popularity of raw food and the growing cat population across Europe.

Garyth Stone, Managing Director in Houlihan Lokey’s Consumer Group – a US-based investment bank and financial services company – attributes the force of the industry to its “strong” fundamentals. “That’s the main driver: increased spend per pet rather than increased number of pets,” he says in an interview with PETS International.

This market is heating up due to the changing behavior of pet parents and the arrival of a new generation that is more focused on high-quality pet food. “All of that is feeding into higher-quality, more expensive, higher-margin products,” states Stone.

Strengthening segments

Fresh pet food is one of the areas with the most activity so far this year due to a combination of opportunity and caution. “The bigger companies can’t quite predict how big the segment will become and they are trying to decide if it is worth it to invest. So we’re seeing a lot more from an acquisition standpoint in that sense,” says Andrea Binder, Pet Industry Thought Leader at market research firm NielsenIQ.

The next strongest segments are veterinary services and pet health, care and pharmaceuticals. Rising vet bills have boosted the deals in this sector, leading to companies trying to offer more affordable services to struggling consumers.

According to Binder, there has been strong deal activity around some science-backed products, such as the supplements category – which is one of the few categories that is growing in store today. “We are seeing a lot of activity there, in manufacturers investing in those supplement companies rather than trying to go get all of the scientific research, which means so much more to the consumer these days,” she comments.

Malmö-headquartered pet health brand Swedencare expanded in March with the acquisition of British player Summit Veterinary Pharmaceuticals for £30 million ($39M/€36M). In another example, US home, pet and garden goods chain store Tractor Supply moved into the online pharmacy space by acquiring Allivet in January.

Focus on efficiency and scalability

Retail businesses, making up 9% of the total investments reviewed, are mainly linked to local distributors, with a focus on scalability and omnichannel strategy.

For Gilles Vanhouwe, Director at Brussels-based investment company Verlinvest, pet retail “continues to appeal to investors on a consolidation thesis”.

In January, for example, Bulgarian pet retailer Petmall announced a merger with its distributor, Petfoodtrade, to form a single entity to improve efficiency in the local pet market. Meanwhile, Dubai-based Pet Corner has expanded its regional presence with the acquisition of another pet retailer, Jungle Paws, based in Abu Dhabi.

Despite that, “many are waiting for a larger catalyst to unlock activity”, Vanhouwe explains. “Direct-to- consumer brands are maturing, with a handful like Katkin breaking into retail, while roll-up platforms such as Nutriment and AlphaPet are emerging as credible players.”

Fewer deals in other areas

Other pet industry sectors witnessing deals this year include accessories and toys (4%), packaging (4%), and wholesale and distribution (4%), as well as wellness, supply, services and tech (2% each).

One of the highlights in the pet tech sector was the acquisition of Mars subsidiary Whistle by the GPS tracking and health monitoring platform Tractive.

According to Verlinvest’s Vanhouwe, besides the big sectors already explained, grooming, specialty retail, and pet pharma and wellness also stand out as “strong growth pockets”.

Consolidation in Europe

With M&A transactions in Europe accounting for 67% of the major deals analyzed, there are signs of strong consolidation on the continent, mainly in the pet food and pet care sectors.

Stone from Houlihan Lokey’s Consumer Group highlights that M&A activity is characterized by waves. The premiumization trend – which dominated the American market and led to many interesting brand acquisitions in recent years – arrived to Europe somewhat later and took more time to grow and consolidate. “It’s only when companies get to a certain scale that they’re therefore relevant for M&A transactions,” he says.

North America accounts for the second-largest number of pet industry investments so far this year, with 17% of the analyzed deals distributed across the US. Extending beyond food to span wellness, veterinary, pharma, accessories and tech, the American investment market indicates a focus on innovation, scale and specialization.

Expansion and emerging markets

The Asia-Pacific region, accounting for 9% of the analyzed deals, is mainly focused on pet food and veterinary services. In the Middle East, Latin America and Africa, which each account for just 2% of the investments analyzed, businesses have mainly been acquired in the retail and pet food sectors.

Some of these moves were motivated by goals of geographic expansion. One example is the $62 million (€53M) acquisition of Australian pet-sitting company Mad Paws by US player Rover in order to gain a foothold in the Australian and New Zealand markets.

Similarly, Nestlé’s and Mars Veterinary Health’s acquisitions of minority stakes in Indian companies Drools and Crown Vet, respectively, are ways for major international players to test new emerging markets.

Investing in M&A for the future

The pet market is clearly still seen as having the potential to generate worthwhile returns. Most recent M&A developments have included investment group Eurazeo’s completion of the sale of Ultra Premium Direct, France’s leading DTC online pet food company, to UK pet food manufacturer Inspired Pet Nutrition.

Similarly, the American firm Central Garden & Pet has pointed to M&A as one of its strategies to recover from its net sales declines at the beginning of the year.

“The pipeline includes a handful of larger processes expected toward the end of 2025 and into early 2026. The outcome of these transactions, in both valuations and investor appetite, will help set the tone for the next cycle of M&A activity in the sector,” concludes Vanhouwe.

Share this story: