Analysis: key trends and challenges in the Russian pet market

With pet food production skyrocketing, the local industry is living through unprecedented times. How is the future looking?

2022 was a year of unprecedented challenges and changes in many ways for Russia, including the pet business.

According to Zooinform, in 2022, the pet market reached a staggering ₽330 billion (€3.31B/$3.39B), registering a 25% increase compared to the previous year.

This growth can be attributed primarily to inflation, with prices increasing by a minimum of 15%. A notable aspect contributing to the price surge is the cost of pet food. The cost of a ton from manufacturers almost doubled between January 2022 and February 2023 and is still going up.

Consumers felt the impact immediately, as retail prices increased by at least 32% between January and October 2022.

Additionally, the National Pet Industry Association (NPIA) estimates that the cost of imported pet food increased by between 30% and 80%.

Local vs. imports

While the pet market has seen substantial growth in monetary terms, its volume expansion was modest.

Imports decreased by 26% in 2022, equating to a reduction of approximately 40,000 tons.

Domestic production grew in 2022 and kept expanding into 2023. In 2022, Russia produced 1.38 million tons of pet food, compared to 1.32 million in 2021 (+4.5%).

This resulted in the volume of locally manufactured pet food going up by 60,000 tons, overlapping the shortage of imports by 20,000 tons.

Made in Russia

Russian pet owners are increasingly inclined to feed their pets locally-produced food.

According to a survey by Zooinform and Four Paws, a major pet retail chain in Russia, 57% of consumers prefer to feed their pets domestic pet food. The trust rate is much lower—25%—and 29% confess they purchase Russian-made food because of imported pet food shortages.

In the face of the new economic reality, pet owners in Russia are more cost-conscious, with 72% indicating the need to economize. Price has become the primary concern for 89% of Russian consumers when making purchasing decisions.

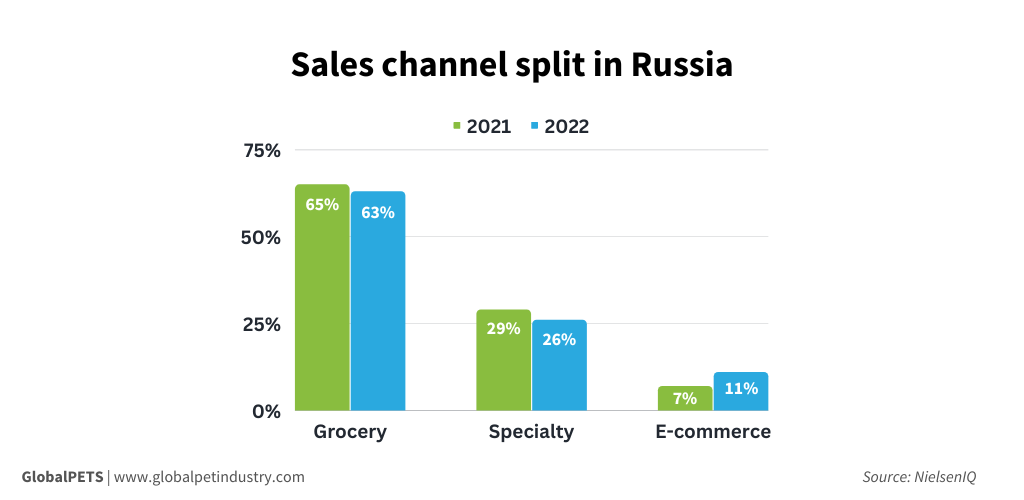

NielsenIQ data reveals that specialty retail and grocery channels lost 3% and 2% of shares, respectively, to e-commerce in 2022. Within the first half of 2023, e-commerce almost doubled its market share, accounting for nearly 22% of pet food sales.

A changing landscape

One of the most significant transformations in the Russian pet market is the rapid development of domestic pet food production. Several major new plants, like Limkorm and AlphaPet, were launched in 2022, and numerous small regional producers emerged all over the country.

The construction of several more large-scale manufacturing plants is underway.

However, the NPIA estimates that to achieve technological sovereignty, Russia needs to establish at least 10 new production facilities with a combined capacity of over 300,000 tons of premium and super-premium products. The total investment required is estimated at ₽50 billion (€478M/$514M).

Significant transformations have also occurred in the veterinary pharmaceuticals market. MSD, the market leader in antiparasitic products, and Zoetis have downsized or closed their pet divisions in Russia.

Boehringer Ingelheim and Elanco remain the only international players in Russia. The market volume for veterinary pharmaceuticals has decreased by 1.2%, amounting to ₽21.3 billion (€203M/$219M), and by 18.4% in volume, reaching 140 billion units.

As of 1 September 2023, only international manufacturers certified with the Good Manufacturing Practice (GMP) of Russia will be allowed to supply veterinary medicines (vaccines and other pharmaceuticals) to Russia. None of the above-mentioned companies have the Russian GMP certificate so far, which may result in an unprecedented shortage of veterinary medicines.

Future forecast

Facing the new reality with various international sanctions, recent import bans from two Italian factories—Monge and United Pets—imposed by the Russian authorities, and the changing economic situation, Russian pet industry players are forced to find ways to continue supplying pets in Russia with the best products possible.

This has led to various companies searching for new economic and logistical ties and partnerships. Pet food from Turkey, China, and Argentina is on its way to Russian retail shelves and pet bowls.

Pet owners continue to be price-sensitive. However, they don’t want to compromise on quality but provide their pets with the best available products they can afford. Nevertheless, according to a recent Zooinform poll, 67% of Russian pet market players stated that sales decreased, 21% managed to keep sales at the same level and 11% declared growth.

Share this story: