Beyond kibble: Inside Europe’s D2C pet food market

New industry data reveals that 5 European countries account for nearly half of all direct-to-consumer pet food brands in the region.

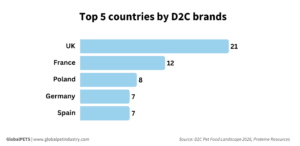

The UK accounts for the largest share of direct-to-consumer pet food brands in Europe, with 21 labels, according to Proteine Resources’ D2C Pet Food Landscape 2026 Report. The study analyzed 113 brands across 28 European markets between May and June.

The UK therefore accounts for 19% of the dataset, with fresh food and subscription-based business models particularly prominent in the market. The median pet food price in the country is €10.95 ($12.81) per kilogram.

France ranks second, with 12 brands (11%) and a median price of €10.16 ($11.89) per kilogram, standing out for its strong focus on dry kibble.

Poland follows with 8 brands (7%), with a notable concentration of fresh pet food brands, with a median price of €10.82 ($12.66) per kilogram.

Although Germany accounts for just 7 brands (6%), it has the highest median price at €13.50 ($15.80) per kilogram, underscoring its position as a premium pet food market, according to the company.

Spain rounds out the top 5, also with 7 brands (6%). It leads the region in raw and BARF (biologically appropriate raw food) diets while posting the lowest median price among the 5 markets: €7.40 ($8.66) per kilogram.

Hidden cost paradox

Following an analysis of more than 9,000 products from the surveyed brands, the report found that a higher price per kilogram does not necessarily translate into a higher daily feeding cost.

For example, raw/BARF has the lowest median price at €7.98 ($9.34) per kilogram but also the second-highest daily feeding cost at €3.59 ($4.20), based on a recommended serving of approximately 450 g per day.

By comparison, dry kibble has a slightly higher median price of €8.24 ($9.64) per kilogram but the lowest daily feeding cost at €1.65 ($1.93), as pets typically consume only around 200 g per day.

The report attributes this difference to feeding volumes. Products with higher moisture content, including fresh, wet and raw diets, require significantly larger daily portions than dry kibble.

Fresh/cooked pet food had the highest median price at €10.68 ($12.50) per kilogram and the highest daily feeding cost at €4.27 ($5), based on an average daily serving of 400 g. Wet food, meanwhile, had a median price of €9.07 ($10.61) per kilogram and a daily feeding cost of €3.17 ($3.71) for an average daily serving of 350 g.

How segments differ

Dry kibble remains the dominant format in the D2C pet food market, accounting for 40 brands and spanning the widest price range, from €1.05 ($1.23) to €66.61 ($77.34) per kilogram.

Supported by its long shelf life, the segment has a 55% subscription rate, with brands competing through personalization and customer loyalty. Non-subscription brands focus on price and purchasing flexibility.

Fresh/cooked pet food has 37 brands and more than 1,300 products. Despite representing roughly one-third of brands, it attracted 73% of all D2C pet food funding, reflecting strong investor interest.

Nearly all fresh/cooked brands (89%) operate on a subscription model because the products are perishable, the company states.

Wet pet food is the smallest D2C segment by brand count (10), with more than 400 products. It has a 60% subscription rate, largely driven by the convenience of automated deliveries for bulky, heavy products.

Raw/BARF has the lowest subscription rate at 54%. The report says its growth is constrained by logistical complexity, regulatory uncertainty in some markets and the difficulty of scaling artisanal production.

Subscription trends

Overall, 2 in 3 (66%) D2C pet food brands offer either a subscription-first or optional model.

Products in this category are priced 38% higher than those in non-subscription offerings, reflecting the added value of services such as personalized meal plans, automated portion calculations, scheduled deliveries and shopping convenience.

Uneven funding

European D2C pet food brands have raised a combined €811 million ($949M) in publicly disclosed funding to date. Of the 113 brands analyzed, 44 have secured external investment.

Butternut Box is the sector’s most-funded company: it raised €442 million ($517M), representing 55% of all disclosed investment. Together with Ultra Premium Direct, KatKin, Untamed, Pure Pet Food and Edgard & Cooper, the top 6 brands account for 79% of the total.

By segment, fresh/cooked pet food attracted the majority of investment, securing €594 million ($695M), or 73% of total funding.

Dry kibble followed with €140 million ($164M), while raw/BARF brands raised €40M million ($47M), and wet food brands secured €37 million ($43M).

Investment trends

The report notes that venture capital interest in pet food peaked between 2020 and 2022, when the pandemic accelerated both pet adoption and e-commerce growth. Funded brands invest heavily in performance marketing, increasing customer acquisition costs.

Meanwhile, growth-stage investors are increasingly prioritizing capital efficiency, proven unit economics and profitability, making later-stage funding more difficult for mid-sized brands, the report concludes.

Share this story: