Health-driven labels gain ground in Italy’s evolving pet food landscape

A new study shows Italian pet owners are increasingly prioritizing nutritional claims, while interest in locally made products declines.

The Italian pet food market declined in both value (-0.6%) and volume (-1.4%) from June 2024 and June 2025, reaching over €1.2 billion ($1.4B) in sales across 3,913 products.

According to Observatory Immagino by GS1 Italy, a biannual study analyzing Italian consumer goods by tracking label data, this decline was attributed to a moderate inflationary environment (+1.5%) and a contraction in demand (-2.8 percentage points).

The performance was partially offset by increased supply (+2.3 points) and higher promotional pressure (+1.8 points), which reached a 22% share.

The study covers more than 100,000 fast-moving consumer goods (FMCG) products in Italy.

Results by pet type and category

The cat food segment, which, according to the report, generated €800 million ($926M) in sales in Italy during the period, contributed positively in volume (+0.2%). Results were driven by strong snack performance, which grew 7.7% in value and 5.3% in volume.

Meanwhile, the dog food segment generated roughly half of its revenue, €406 million ($470M), and saw a 4.5% decline in volume.

Snacks were the most dynamic category across the market, generating €211 million ($244M) in sales. Within dog food, snacks grew 1% in value and 2.2% in volume.

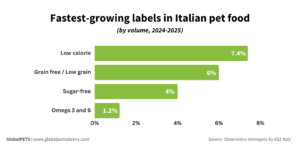

Top-growing labels

The study analyzes the performance of specific labels and identifies the most popular and fastest-growing features in dog and cat food.

For instance, low-calorie products recorded the strongest volume growth, with sales rising 7.4%, followed by grain-free or low-grain products at 6%, sugar-free at 4% and Omega 3 and 6 at 1.2%.

In contrast, several labels declined. Products featuring fresh meat or fish fell by 9.9%, while those rich in fiber declined by 2.6%. Italian-origin labels dropped 2.3%, and products rich in vitamins decreased by 2%.

According to GS1 Italy, these trends reflect broader shifts in human nutrition, including a growing focus on well-being and nutritional balance, increased attention to sugar and calorie intake and support for intestinal and cardiovascular health.

‘Free-from’ performance

Free-from products remain the largest segment in the pet food market, with 1,997 offerings generating more than €723 million ($837M) in sales.

In this segment, sugar-free products account for the largest share, with 541 products generating nearly €211 million ($244M) in sales. The category was driven by both supply expansion and promotional activity.

Then came low-calorie items, which represented 76 SKUs and generated nearly €46 million ($53M) in sales. Finally, sales of grain-free and low-grain products exceeded €42 million ($49M).

‘Rich-in’ revenues

The rich-in segment, comprising 1,968 products, generated more than €650 million ($752M) in sales across dog and cat food.

Products rich in vitamins represent the largest sub-segment with 1,226 SKUs and over €435 million ($503M) in sales.

Those offerings containing prebiotics recorded solid growth, reaching 247 products and generating nearly €117 million ($135M) in sales, supported by expansion in shelf presence.

‘Made in Italy’

Pet food products carrying Italian-origin labels, covering 521 SKUs, appear to be losing appeal among consumers, with demand declining by 6.2 percentage points (p.p.) over the past 12 months.

An increase in supply of 4.2 points was not enough to offset falling sales, which declined by 2% in value and 2.3% in volume, bringing total turnover to below €121 million ($140M).

Similarly, other origin-related claims–including products featuring the Italian flag (505 SKUs), “100% Italian” (33 SKUs) and “Italian quality” (19 SKUs)–also recorded declines in both value and volume, driven by weaker demand.

Only the “Made in Italy” claim showed positive performance. Found on 382 products, it generated more than €86 million ($100M) in sales, with both value and volume increasing by 0.6%.

E-commerce

The e-commerce channel in the fast-moving consumer goods (FMCG) sector generated around €1.3 billion ($1.5B) in sales, with value growth of 5.9% and volume growth of 5.3% in the year to June 2025.

This represents significantly stronger performance compared to physical retail channels–including hypermarkets, supermarkets and small self-service stores–where sales increased by 1.8% in value but declined by 0.4% in volume over the same period.

The report concludes e-commerce growth is supported by the availability of detailed digital product information on major platforms, making it easier for consumers to identify products that meet specific needs.

Share this story: