H2 economy outlook: Tech investment and consumer resilience amid global challenges

Economists expect growth to be uneven, driven by AI expansion. In the pet sector, strong fundamentals and adoption rates will likely boost investments.

As we reach the middle of July and pass the middle of the year, economists around the world are piecing together what went right and wrong in the first half of 2026 while trying to predict the direction of growth, inflation, interest rates and consumption in an uncertain scenario.

Uneven growth

Investment bank J.P. Morgan points to a paradox: price shocks from the war in the Middle East will persist, but not enough to undermine growth.

“Markets will continue to navigate the tension between the ongoing energy supply shock and a resilient growth backdrop, supported by improved labor markets and AI-related capital spending,” says Hussein Malik, Head of Global Research at J.P. Morgan.

Data from the world’s largest economy corroborates the positive sentiment. According to Danske Bank Asset Management, even after the shock of the war against Iran, the US continued to accelerate its gross domestic product (GDP) growth by about 2.5% month-over-month (MoM).

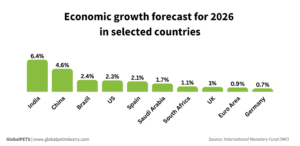

The global path will, however, be uneven. The International Monetary Fund (IMF) projects global growth of 3% for 2026, but says that while investments and demand in AI are boosting countries integrated into this development, the shock from the war is affecting energy importers and vulnerable economies more heavily.

Examples include: the Eurozone is projected to grow by 0.9%, with Spain performing better (2.1%) and Germany staying at 0.7%; the UK is expected to grow by 1%, while China (4.6%) and India (6.4%) have more positive forecasts.

Improving consumer sentiment

Based on a survey of 30 countries to compose Ipsos’ Consumer Confidence Index, the market research and consulting firm found that consumers’ perceptions of the economic climate and their current purchasing, jobs, and investment confidence were up 0.7 percentage points (p.p.) in June.

Their expectations about future economic conditions declined by 0.4 p.p., indicating that consumers are positive but cautious about the future.

Analysts from the Bank of America (BofA) say that higher asset values and wage gains in the US will sustain consumption. But although American consumers have an above-average positive sentiment, Ipsos’ ranking is headed by India, Sweden, Malaysia, Colombia and Brazil.

On the other hand, Chile, France, Japan, Argentina and Türkiye show the weakest consumer sentiment among the surveyed countries.

This resilience was translated into a 2.7% rise in global real retail sales, excluding China, according to J.P. Morgan. “However, the strength of the consumer could be called into question in the coming months if inflationary pressures persist, especially if energy bills spike further,” the company states.

Inflation and interest rates

The investment bank expects inflation to remain high overall, followed by “uneven and gradual hikes” in interest rates “from developed market central banks.”

First things first: global average core inflation is forecast to remain close to 3%. The rise is attributed to high demand, supply chain struggles (especially in the tech sector) and the effect of energy price pass-through.

But even in the face of increases, J.P. Morgan says that central banks’ policies have been one of patience. In their last meetings in June, the US and the UK kept rates unchanged, while Europe raised them by 25 basis points.

“Even with expectations for rate hikes in the coming months, we anticipate global policy rates to rise less than 20 basis points (bp) over the course of this year,” says Chief Global Economist Bruce Kasman.

Equity market and company results

An analysis from financial services company Allianz says that while most sectors posted positive earnings per share (EPS) growth in the first quarter of 2026, “turnover growth was revised down for 12 out of 16 sectors, led by pharma, utilities and motor vehicles.”

According to Allianz, electronics, information and communication services, and food and beverage are the sectors expected to keep generating profit this year.

Regardless of whether profitability becomes more widespread, the stock market will continue to grow. “While it feels like a disconnect, markets aren’t ignoring bad news. Instead, sound economic fundamentals are enabling markets to see past today’s turbulence to potentially transformative growth ahead,” Chris Hyzy, Chief Investment Officer for Bank of America Private Bank, notes.

Bo Bejstrup Christensen, Head of Macro at Danske Bank Asset Management, points to positive expectations in emerging market equities. This is especially pronounced in South Korea and Taiwan, which are benefiting from increasing US capital expenditures to build AI capabilities, although the Brazilian stock market is also going up.

“The core of the second half will be determined by the strength of the US expansion,” Christensen says, which will lead to growth in equities. Goldman Sachs Research raised its S&P 500 forecast for 2026 to 8,000 in May, up from 7,600 in an earlier projection. As of 10 July, the index is 7,575, according to S&P Global.

What to expect in the pet market

Representative entities in the pet sector across different countries expect industry growth to accelerate this year. In the US, the American Pet Products Association (APPA) projects a 0.7 p.p. increase in growth by 2026 (4.4%) compared to 2025 (3.7%). Brazil also expects higher growth in 2026 – 4.2% compared with the 3.6% recorded last year.

According to Cascadia Capital, “The category is ripe for continued growth as adoption rates remain healthy, humanization and premiumization trends continue, and new innovation fuels a focus on longevity and ‘healthspan’ among other drivers.” The company evaluates the US sector, but the trends resonate with other markets as well.

For Anna Skaya, General Partner at the venture capital fund AniVC, on the consumer side, growth will be driven by sustained consumption by “higher income and premium pet owners,” contrasting with “owners at the bottom trading down to value brands and stretching out purchases.”

More deals to come

Positive outlooks, together with investment cycles, will likely contribute to an uptick in mergers and acquisitions.

“M&A activity is heating up in 2026 following a 3-year period of minimal transaction activity; operators have greater visibility on their businesses, various COVID-era sponsor deals are ready for liquidity events and institutional investors continue to look closely at new pet investment opportunities,” the Cascadia Capital’s Pet Industry Insights report says.

The investment bank expects deals including Honest Kitchen, Nulo, Stella & Chewy and Weruva, while Open Farm is exploring an initial public offering (IPO).

Skaya tells GlobalPETS that dry powder (cash reserves or liquid assets ready for investment) is at “record levels,” and investors “still love this category for its long-term tailwinds.” In the US, private equity middle market dry powder has jumped 26.6% between 2021 and 2025, according to Cascadia’s report.

“We see continued momentum within the pet sector and are particularly bullish on super premium alternative pet food, pet supplements, and pet technology as high-conviction categories for investors. These segments are demonstrating durable demand and structural growth that transcends near-term macro volatility,” Christoph Wunn, Director of Consumer Products and Services at the investment bank William Blair, tells GlobalPETS.

Although inflation, interest rates and geopolitical tensions are putting pressure on markets, resilient consumer demand and continued investment indicate an opportunity for the pet industry in premium offerings, innovation and strategic expansion.

Share this story:

One click prioritizes GlobalPETS in your search results and AI answers.